2025 Tax Cliff: ‘Death Taxes’ Threaten Farm Families

Samantha Ayoub

Economist

The Dec. 31, 2025, expiration of many provisions of the 2017 Tax Cuts and Jobs Act (TCJA) adds a new task to the 2025 congressional to-do list: updating the tax code. Many TCJA provisions provided important relief for farm families. While reductions in the corporate income tax rates were made permanent in 2017, income tax cuts for individuals began to phase out in 2022, with the biggest tax increases coming with expirations at the end of 2025. This Market Intel report is the fourth in a series exploring the expiring TCJA provisions – including individual tax provisions, the qualified business income deduction, capital expensing provisions and estate taxes – and their impact on farm families.

For some families, grieving the loss of a loved one comes with an added burden: a hefty tax on everything their family member left to them.

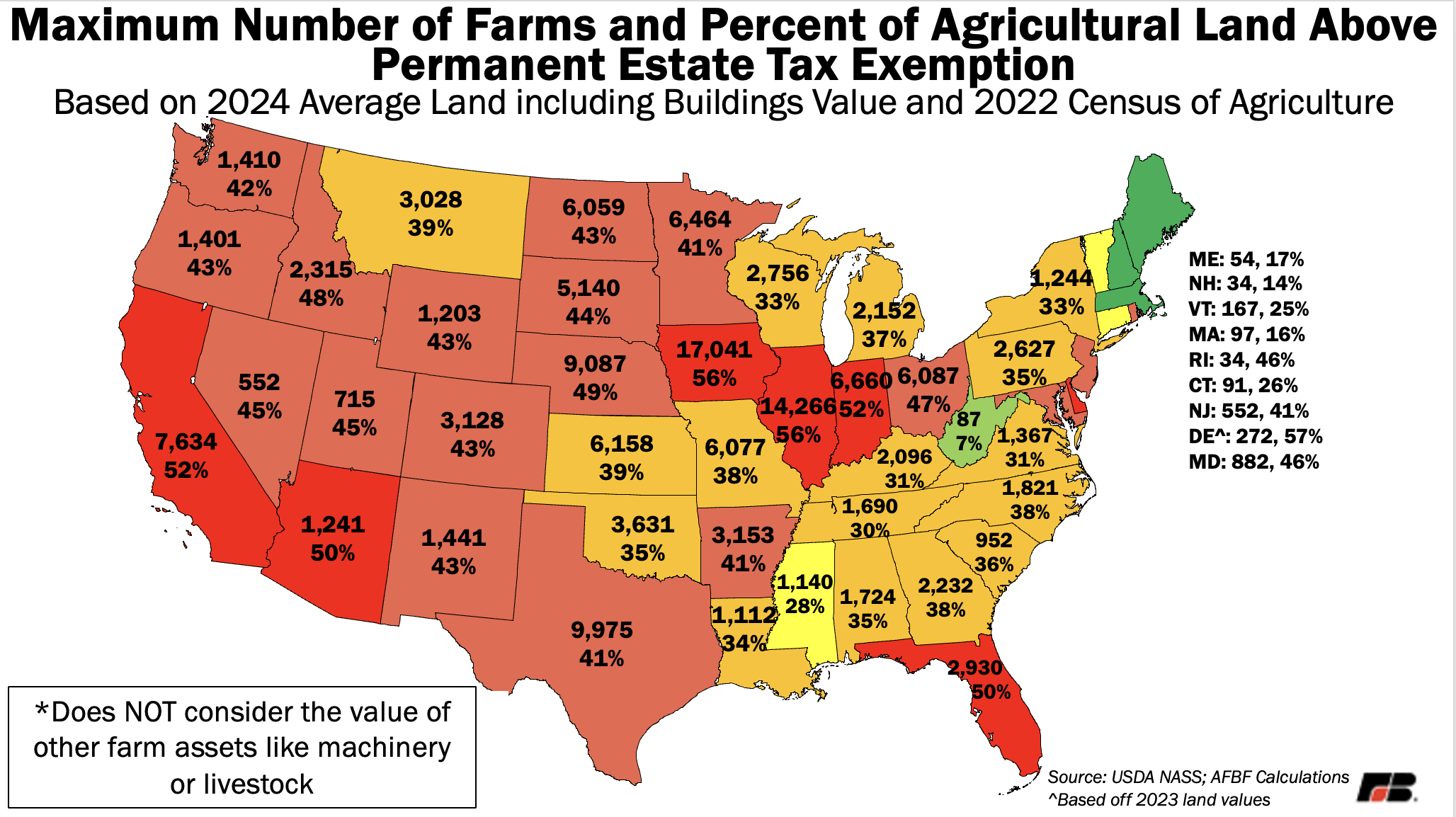

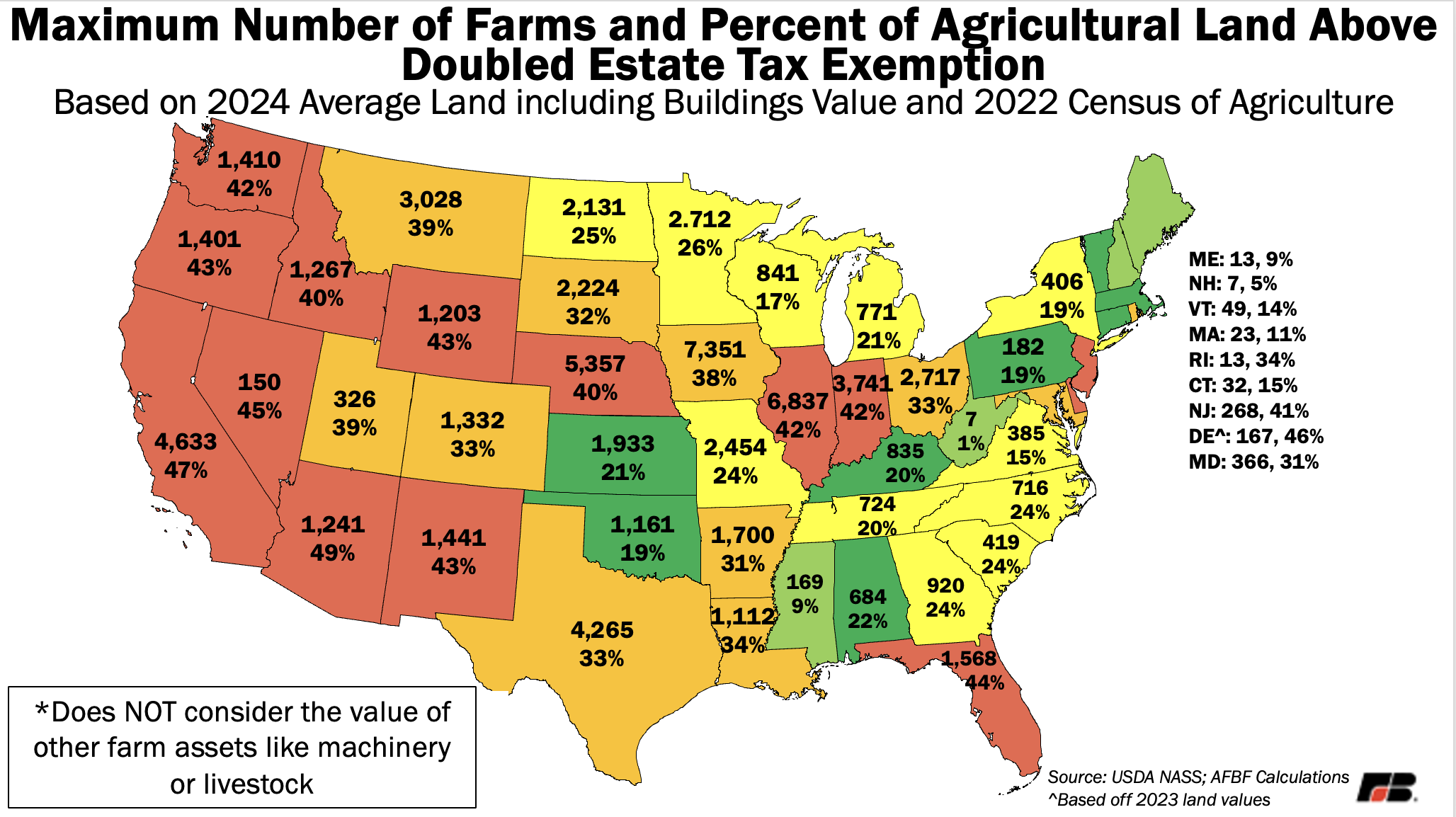

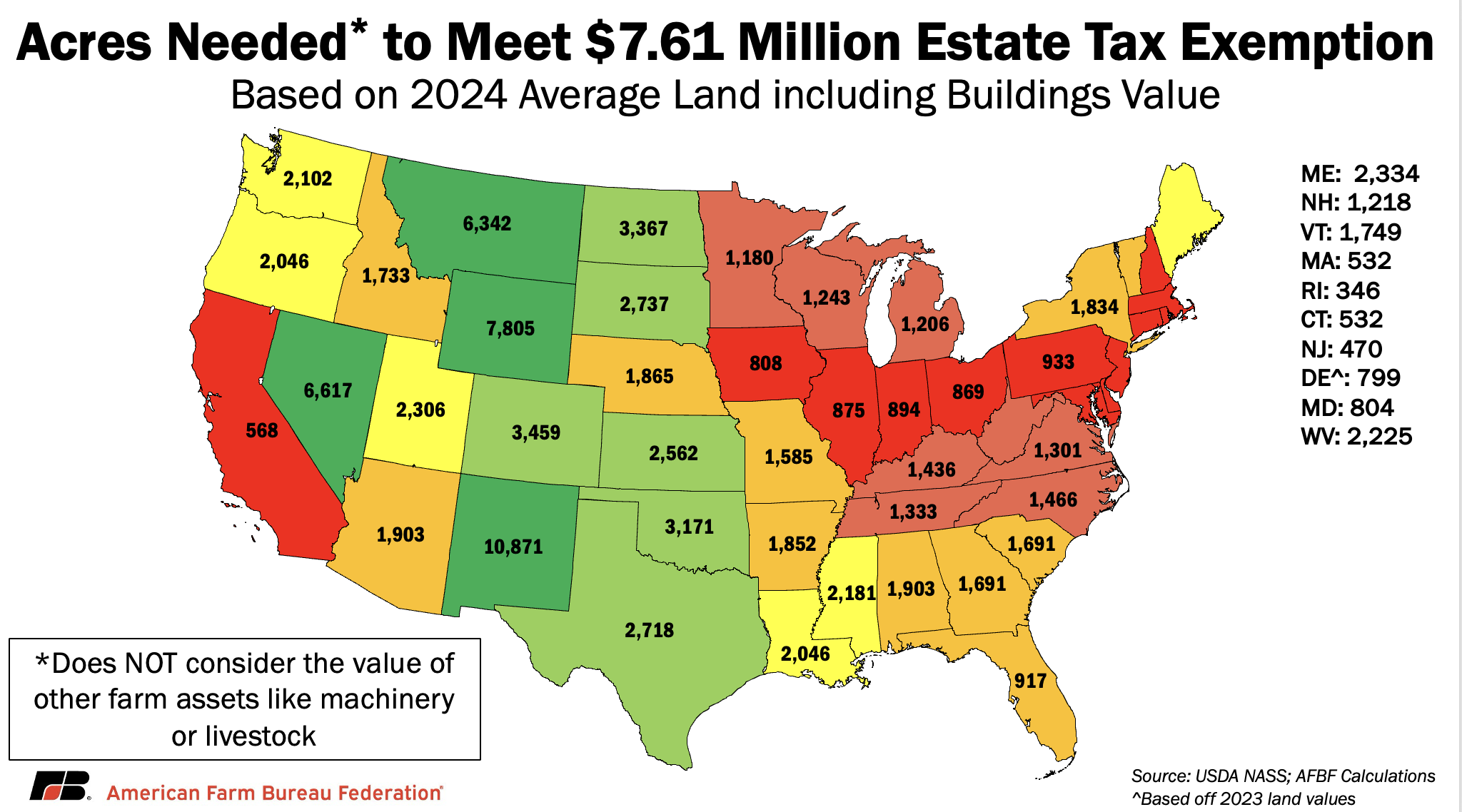

The estate tax, also called the “death” tax, turns a time of mourning into a race against time to pay a government bill. Exactly nine months after the death of a family leader, some farm families owe the Internal Revenue Service (IRS) up to 40% of their farm’s value above an exemption limit. Without an act of Congress this year, the estate tax exemption will drop by 50% to $7.61 million on Jan. 1, 2026, putting the future of thousands of farm families at risk. While these may seem like big numbers, most of the value of a farm is tied up in land and expensive machinery, which are needed to grow food and raise animals. Actual cash on hand is much lower, making payment of exorbitant taxes extremely difficult or even impossible.

Who Pays for Dying?

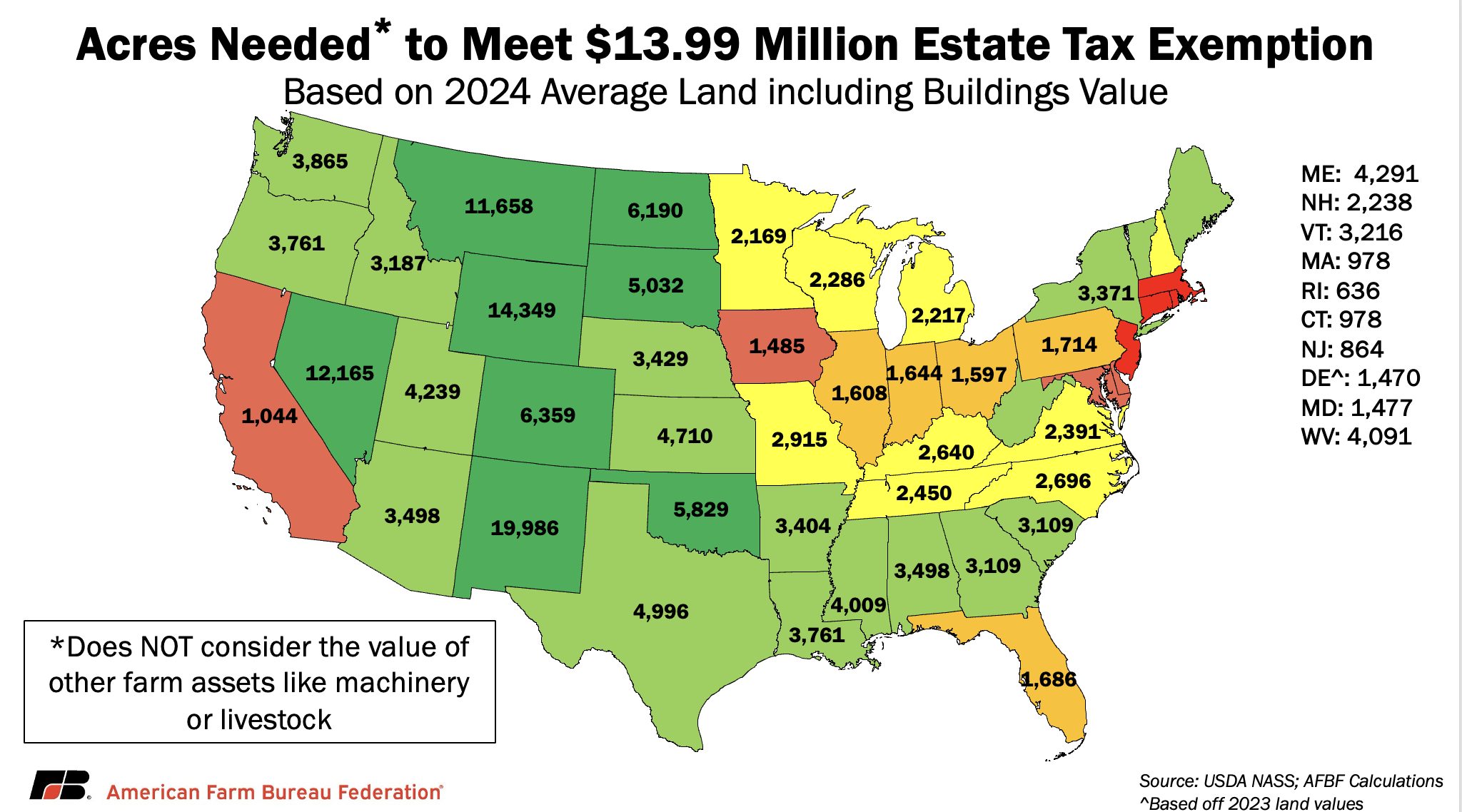

The TJCA doubled the estate tax exemption from $5.5 million per individual to $11 million indexed for inflation. Property left to a spouse transfers without an estate tax, which can effectively double the estate tax exemption when a surviving spouse passes. That means that in 2025, the estate of any farmer or rancher with a net worth over $13.99 million, if owned by an individual owner, or $27.98 million if owned by a married couple, must file an estate tax return within 9 months of their passing.

Just last year, USDA estimated that if the estate tax exemption reverts to its pre-TCJA level, nearly twice as many farms in every sales class would have to pay estate taxes. The average net worth of farms subject to the estate tax would be lower under the permanent exemption level –falling from $32.5 million at the higher exemption to just under $20 million, meaning more smaller farms would be impacted. Low sales farms – who have a farmer whose primary job is farming but have an average loss of more than $5,700 a year – would see the sharpest fall in net worth, going from $42.5 million to only $19.5 million. This is because all farms, regardless of their size, operate with high-value land and machinery.

The Value of Land

An estate covers the entirety of someone’s worldly possessions: land, machinery, cash, crops in storage, livestock, business interests and the family home. Farm families’ net worth is typically tied up in illiquid assets like those mentioned above. Over 80% of an average farm’s assets are in real estate alone. This means farmers and ranchers have to plan ahead – or scramble during an already devastating time – to acquire enough liquid cash to pay an estate tax bill.

Agricultural land continues to grow more valuable, which helps farmers obtain credit during a down economy but also pushes more farms’ net worth over the estate tax exemption. In 2024, the national average value for agricultural land, including buildings, was $4,140 per acre. This is more than 37% higher than when TCJA was passed in 2017. That means only 1,800 acres, on average, would be needed to reach the lowered estate tax exemption of $7.61 million after indexing. In states with high-value cropland, farms with as little as 350 acres might be liable for estate taxes. These may seem like large properties, but an 800 acre corn farm in Iowa would earn $600,000 in farm revenue from 2024 corn prices, and with rising expenses, would actually face losses of over $150,000. Even when prices were high in 2022, a typical 800-acre corn farm in Iowa only made profit of $162,000, on a very large asset base. That income goes towards both business and household expenses, and revenue could be split between multiple families. Farmers typically earn lower return on their capital, including the land, than most investors, which makes paying estate taxes particularly difficult for farm families.

With other high-value assets besides land, including machinery, many farms would face estate taxes well before reaching this acreage. The average net worth of an American farm family was $2.5 million in 2023, including all farm and non-farm income. On the average farm, $1.8 million of that is in just the agricultural land and buildings.

Special Use Valuation

Farmland is valued differently than land for other uses like housing developments, shopping malls or solar fields. The Internal Revenue Code determines the agricultural value of farmland using cash rents for similar properties and the Farm Credit System interest rate. Typically, they find farm values to be one-third to one-half of other market values.

Section 2032A protects farmland from being swept into estate taxes based on higher development values for that land. This provision is specifically for farmers and ranchers who have a majority of their net worth in farm assets. If they owe an estate tax after death, the executor can deduct up to $1.42 million of land value from their net worth in 2024. Families who use this deduction commit to continue farming for at least 10 years without harvesting timber or selling off conservation easements, putting additional limits on their ability to come up with cash to pay their estate taxes. If they sell the farm or go against the limits on land use, the family will have to repay the deduction amount.

Stepped-Up Basis

Basis is the purchase cost of an asset. If a long-term asset is sold for more than the purchase price, taxpayers typically pay a capital gains tax on the difference in value. This tax could be as high as 20% for high-income taxpayers.

Many farms are faced with the hard choice to sell off their land or other assets to pay estate taxes. As we’ve discussed, farmland continues to gain value. If a farmer sells farmland today that has been in their family for 100 years, the value would be far above the original basis, if the original basis could even be calculated. Step-up in basis prevents families from having to pay capital gains taxes on top of their estate tax, if they have to sell the land. To protect inheritors, the government has allowed each generation to “step-up” the basis of their assets to current market value at the time of their inheritance.

The step-up in basis provision has existed nearly as long as the estate tax itself, with each being established in 1921 and 1916, respectively. The provision was repealed in 1976 but reinstated in 1980 partly because of the difficulty of record keeping for property that has been held for generations. However, repealing stepped up basis continues to be discussed on Capitol Hill. This would greatly hinder farmers and ranchers’ ability to pass on farms to the next generation or even be able to sell enough assets to pay their estate tax. Because so many farmers keep their business in the family for generations, they are at particular risk from the loss of stepped-up basis.

Conclusion

U.S. farms are closing and consolidating at an alarming rate, with more than 140,000 farms shuttering between 2017 and 2022 and another 20,000 farms lost in the past 2 years, according to USDA. At the same time, the average farm size grew by 20 acres, putting more farms in the estate tax’s crosshairs as both farm size and land values climb. Since the last time American Farm Bureau economists analyzed the impact of the estate tax, roughly 10,000 more farms and 87 million acres of agricultural land are in farms liable for estate taxes from land value alone. If a family is forced to sell off its farm piece by piece in order to pay an estate tax, they run the risk of eventually losing the farm altogether.

Beyond the impact on individual families, farm succession is critical for ensuring future farm production we all rely on. The turnover of a farm or ranch from one generation to the next requires difficult conversations and extensive planning to set up the family for success. Farmers face uncertainty in many forms, like weather, markets and costs. Providing certainty to the estate tax going forward can lessen the burden of keeping the farm in the family while facing these day-to-day challenges during a difficult time.

Top Issues

VIEW ALL