2025 Tax Cliff: Section 199A Qualified Business Income Deduction

Samantha Ayoub

Economist

The Dec. 31, 2025, expiration of many provisions of the 2017 Tax Cuts and Jobs Act (TCJA) adds a new task to the 2025 congressional to-do list: updating the tax code. Many TCJA provisions provided important relief for farm families. While reductions in the corporate income tax rates were made permanent in 2017, income tax cuts for individuals began to phase out in 2022, with the biggest tax increases coming with expirations at the end of 2025. This Market Intel report is the second in a series exploring the expiring TCJA provisions – including individual tax provisions, the qualified business income deduction, capital expensing provisions and estate taxes – and their impact on farm families.

TCJA created a brand-new deduction for pass-through businesses – those taxed on business profits in the individual income tax system: the qualified business income (QBI) deduction (QBID), commonly known as “199A” for its section in the U.S. tax code. As we discussed in our last Market Intel on the Tax Cuts and Jobs Act, individual income tax provisions are crucial to farm families who operate pass-through businesses. TCJA permanently lowered the corporate tax rate from 35% to 21%, but pass-through entities are at a disadvantage when their individual income rate cuts expire at the end of 2025. The 199A deduction reduces the amount of farmers’ business income subject to tax to provide more consistency with corporations’ effective rates. For the nearly 98% of family farms that operate as sole proprietorships, partnerships or S corporations, USDA’s Economic Research Service (ERS) estimates that 199A is the single-most impactful tax provision for farm businesses when evaluated separately from other TCJA provisions.

How it Works

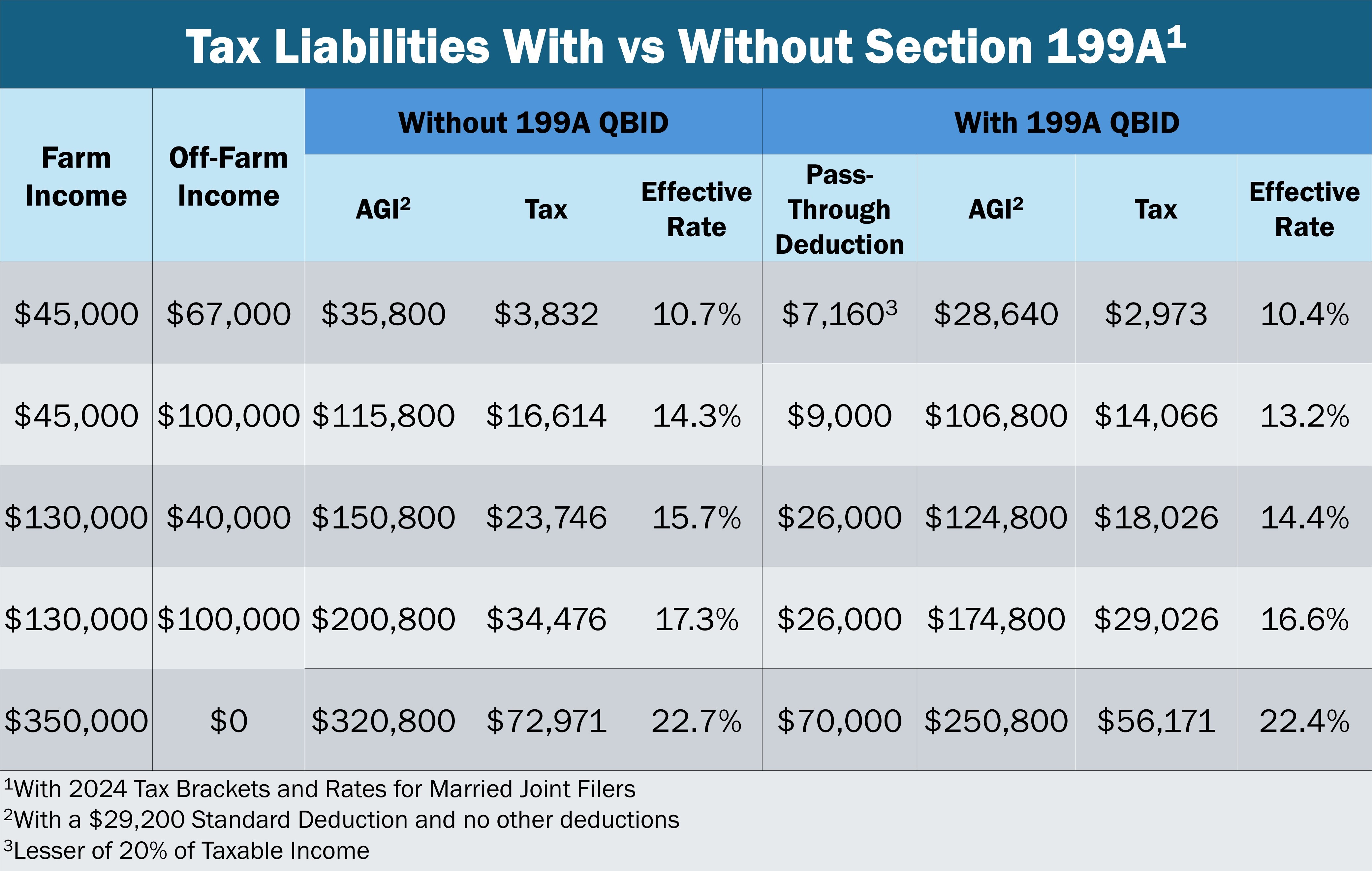

QBI includes the income, minus wage income, deductions, applicable gains and losses, for every eligible pass-through business that a taxpayer operates in the United States or Puerto Rico. This income also includes cooperative payments. Cooperatives operate under a unique structure where the deduction is either retained by the cooperative or passed through to members based on business conducted with or through the cooperative and used to offset the farmer's tax liability. Under the Section 199A QBID, small business owners are eligible to deduct 20% of their QBI from their individual income – or 20% of their total ordinary taxable income if it is less than their QBI.

Section 199A thus lowers pass-through owners’ effective rates so they’re more on par with the permanently lowered corporate rates. It lowers the average pass-through entity’s effective rate to 27.4% compared to a C corporation’s minimum 24.8%. Without the 199A deduction, this gap expands as the owners of pass-through entities would have an average effective rate of 32.9%. For pass-through entities in the top tax bracket, the deduction reduces the maximum effective rate to 29.6%, over 7% lower than the top marginal tax rate for other individuals.

Limits to the Deduction

Two key restrictions on the QBI deduction take effect once the business owner’s income exceeds $191,950 or $383,900 for single or joint filers, respectively, in 2024 before the QBID is applied. While QBI deductions are straightforward before this threshold, calculating the deductions with restrictions can make 199A a complex system.

The first restriction is designed to target business income that is generated from personal skills, known as a specified service trade or business (SSTB). These businesses include accounting, athletics, consulting, financial services, commodity trading and more. In these occupations, the owner and employee themselves are considered the primary asset.

Next is the wage and qualified property (WQP) restriction, aimed at businesses that receive income from largely tangible assets like real estate. The WQP limits the QBID to the greater of 50% of the owner’s share of W-2 wages paid by the business or 25% of those wages plus 2.5% of the owner’s share of the original purchase cost – known as unadjusted basis – of the business’s depreciable assets, including equipment and real estate.

These restrictions are phased in gradually between the lower threshold until the business owner’s income exceeds $241,950 or $483,900 for single or joint filers, respectively, and the restrictions take full effect. When the business owner’s AGI exceeds the upper threshold, no income from a SSTB is eligible for the 199A deduction and the full WQP limitation takes effect.

The most difficult use of the QBID occurs when an owner’s income falls between the lower and upper bounds of the deduction. In this phase-in threshold, the 199A deduction is limited by a reduction percentage (RP). The RP is the owner’s AGI minus the lower threshold ($383,900 for married, joint filers and $191,950 for single filers), divided by 50,000 for single filers or 100,000 for joint filers. SSTB income and WQP value are both reduced by this RP over the span of the threshold, reducing the total deduction.

Impact

More than 25.9 million businesses nationwide claimed a 199A deduction on their tax returns in 2021. The QBID is estimated to support over 2.6 million workers and generate $325 billion of GDP each year by allowing business owners to retain more of their revenue for business investments, thanks to a reduced tax bill.

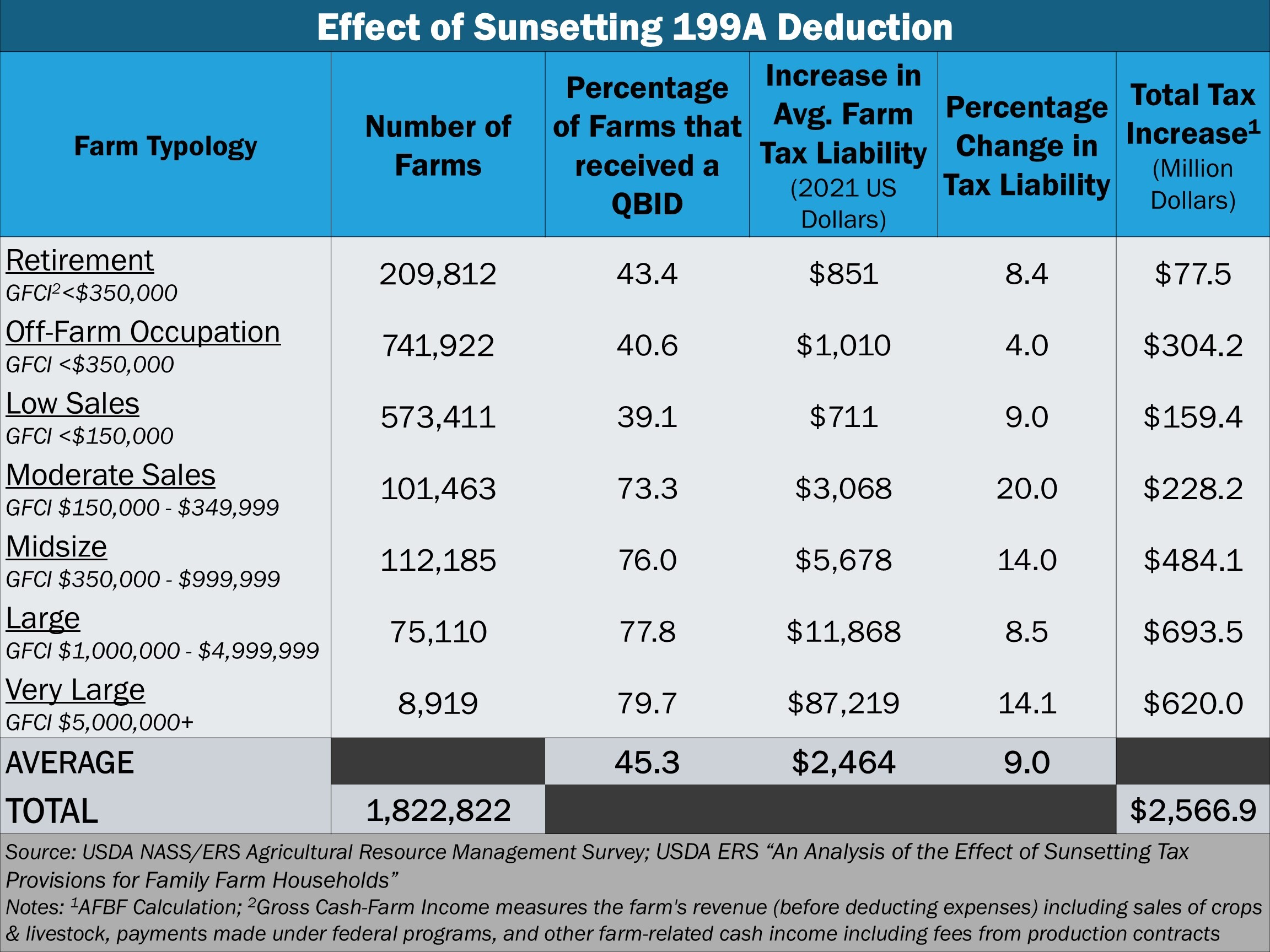

According to ERS, more than 45% of all farm families – over 850,000 farms and ranches – claim the 199A deduction. This jumps to over 70% of farms and ranches where the principal operator is primarily a farmer or rancher, rather than also working an off-farm job. If the deduction were to expire at the end of 2025, a farmer’s average tax liability would increase by $2,464, a 9% increase over their tax bill with the deduction. Similar to the impact of expiring individual income provisions, very large farms would have the largest dollar-value increase in tax burdens – more than $87,000 a year, a 14% increase – but farmers with moderate sales would have the biggest percentage increase in their taxes at over 20% ($3,100 a year). Large farms would have the smallest percentage change in their tax liability, an 8.5% increase, which is one-seventh that of very large farms’ increase (less than $12,000 a year compared to a very large farm’s $87,000).

However, the number of farms in each category, and thus how many are impacted by these tax increases, varies drastically. Low sales farms have the lowest rate of claiming the QBID at only 39%, but that is still over 224,000 farms and ranches claiming the deduction annually. Nearly 80% of very large farms utilize 199A deductions: approximately 7,100 farms. The most farms of one category utilizing 199A are those where the primary operator has a primary job off the farm (“off-farm occupation farms”). More than 300,000 off-farm occupation farms claim 199A and would have an average tax increase of more than $1,000 a year. Seventy-three percent of moderate sales farms claim the deduction, meaning more than 74,000 farms in this category could see their tax bills increase if the provision expires at the end of the year.

The combination of TCJA individual income provisions have the biggest impact on farm and ranch tax billsbecause they impact nearly all farms and ranches, but qualified business income deductions provide the largest reduction in individual farms’ tax liabilities of any standalone tax provision. The average tax increase for all farm categories except for off-farm occupations if 199A were to expire is more than their increase under expiration of other individual income provisions including lowered tax rates, expanded brackets and changes to income deductions and exemptions. Very large farms’ tax increase from 199A’s expiration is more than three times higher than from other income provision expirations. In total, farmers and ranchers nationwide would pay more than $2 billion more in taxes if 199A were to expire.

Conclusion

With over 98% of farms and ranches operating as pass-through entities, few farm operators benefitted from the permanent decrease in corporate tax rates. To provide some parity for small businesses, including farmers and ranchers, the Tax Cuts and Jobs Act created the Section 199A qualified business income deduction.

While it is still unclear what route Congress will take to pass a tax bill this year, legislation to make Section 199A permanent has already been introduced in both chambers of the 119th Congress, with support from more than 230 organizations across all sectors of the economy, including the American Farm Bureau Federation. More than 850,000 farms and ranches nationwide have a lower tax bill under the provision, and out of all the TCJA tax provisions, 199A’s expiration could cause the single largest tax increase for farm and ranch families in 2026.

Top Issues

VIEW ALL