Cattle Inventory Continues Contraction

TOPICS

Cattle

Bernt Nelson

Economist

USDA’s January Cattle Inventory report shed some much-needed light on the state of the cattle industry in the United States. USDA’s National Agricultural Statistics Service (NASS) previously published two semiannual reports on the total inventory of cattle and calves in the United States. In 2024, NASS cancelled the July report, removing critical transparency from the cattle markets. Market analysts, farmers and other stakeholders have been awaiting this report and the overdue information it contains.

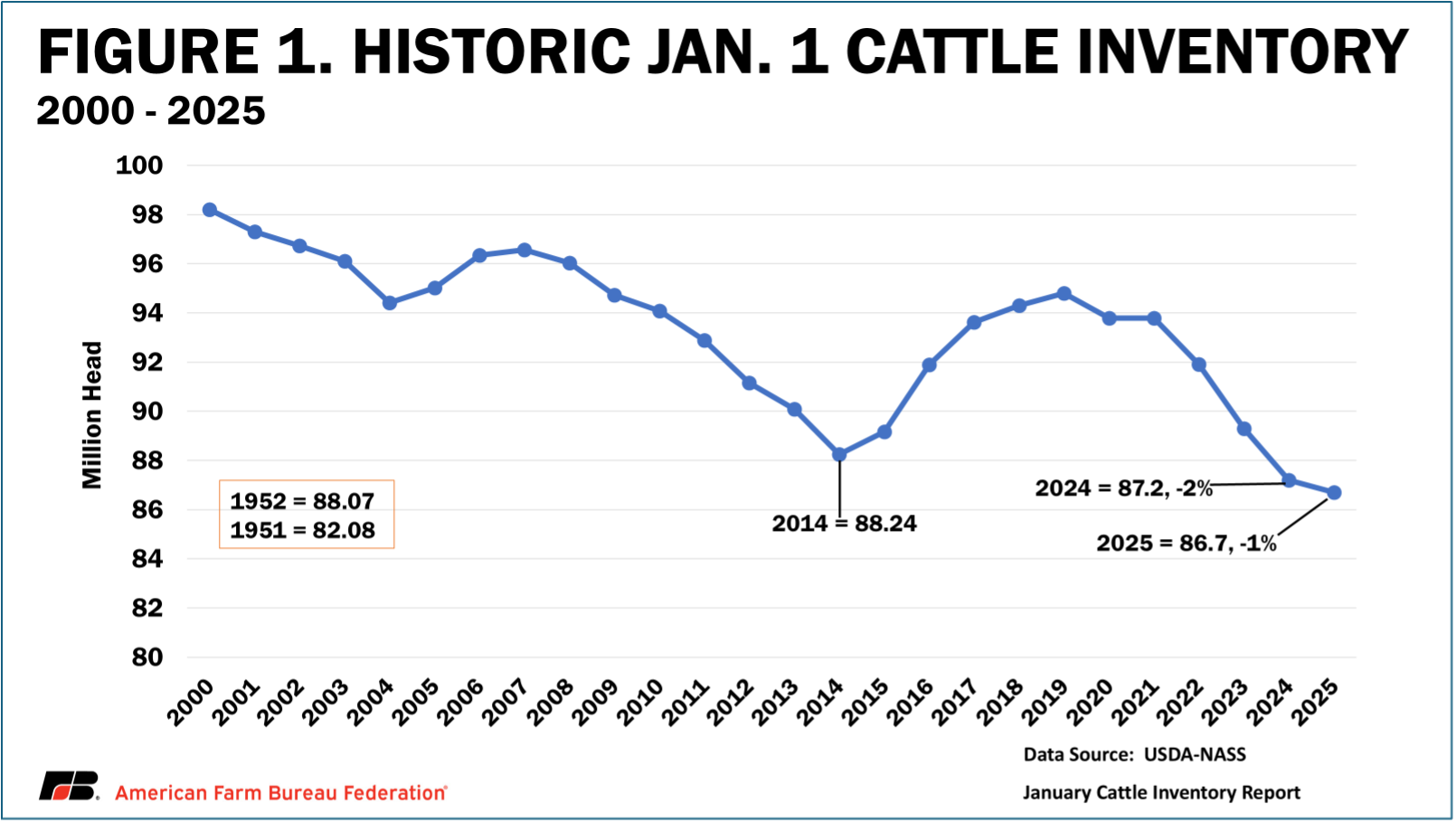

Cattle Inventory

According to the report, all cattle and calves in the United States on Jan. 1, 2025, totaled 86.7 million head, down about 1% from 87.2 million in 2024. The inventory, along with nearly all other estimates in the report, fell within the range of analyst estimates. The decrease, while smaller than last year, indicates continued contraction in the U.S. cattle herd.

Beef cows that have calved totaled 27.9 million, down 1% from 2024 and a new record low (since 1965). Heifers for beef cow replacement were 4.67 million, down 1% from 2024. Heifers for beef cow replacement expected to calve were 2.92 million, down about 2%. Lower numbers for both beef cows that have calved and beef cows expected to calve provide additional evidence of continued herd contraction.

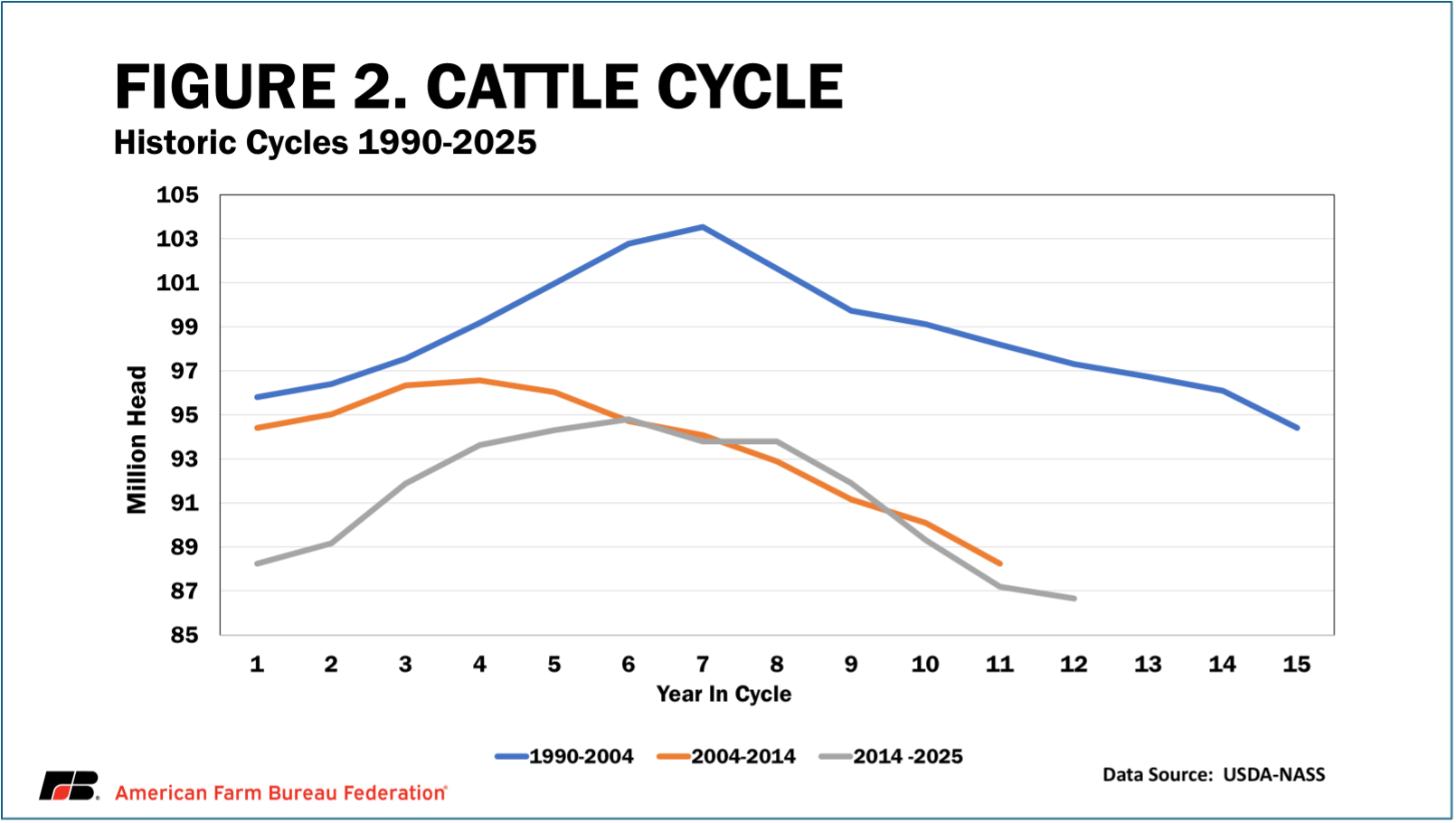

The Cattle Cycle

The cattle cycle is the waves of expansion and contraction of the total number of U.S. beef cattle in consecutive years. The cattle cycle is a response to farmers’ and ranchers’ perceived profitability of the beef cattle industry over roughly a 10-year period. Now in year 12 of the contraction phase, analysts and stakeholders have been waiting for indicators of the beginning of the expansion phase.

Answers in the Calf Crop

The 2024 calf crop was estimated at 33.5 million calves, unchanged from 2023. Ranchers’ decisions on whether to place this calf crop on feed or hold back greater numbers for future breeding will dictate whether the U.S. cattle herd turns toward expansion or continues contraction. Prices for fed steers have already set records in 2025. When combined with lower feed costs, this makes placing cattle on feed, including the calves from 2024, a profitable decision. However, calf prices are also strong, which presents an opportunity for cow-calf producers. If these calves are retained or sold for breeding, it will remove more cattle from the beef market and tighten supplies further before possible expansion with the 2026 generation of calves. If more cattle are held back, prices for fed cattle, and eventually beef prices, will almost certainly move even higher. If the change is more gradual, prices could be a little steadier. Tariff-induced trade wars are sowing uncertainty for both ranchers and consumers alike. This has the potential to impact demand for beef, and even small changes in demand with such tight supplies could have a big impact on prices.

Conclusions and Cattle Cycle

This was a neutral-to-slightly positive report. The overall rate of contraction of the cattle inventory has slowed. However, factors such as demand, beef prices and trade, among others, will influence producers’ decisions about what to do with their animals. Cash prices for fed steers have recently hit record highs. While high prices help profitability for sellers, it’s important to remember they create obstacles for buyers and can even become a barrier for farmers wanting to expand. This is not a typical cattle cycle where high prices lead to growth in the cattle herd. Prices right now are good and uncertainty abounds. High cattle prices combined with the unpredictability of future prices and profitability could compel farmers to continue marketing a higher percentage of females for beef rather than breeding. If this happens, contraction in the cattle industry will continue along with the current cattle cycle.