Cattle on Feed Remains Elevated, Despite Low Cattle Inventory

TOPICS

Cattle

Bernt Nelson

Economist

Despite the cattle inventory plummeting to the lowest level in 73 years, the number of cattle on feed remains surprisingly strong. The average all-fresh retail price for beef hit record highs in six of the last seven months, while the cash price paid to farmers fell from July to September. Though cash prices have recovered in recent weeks, drought is beginning to emerge, creating more uncertainty in the cattle markets. Without the July report to estimate the cattle inventory and calf crop for the first half of the year, farmers and other market stakeholders will be eagerly awaiting USDA’s January Cattle Inventory report.

Cattle on Feed

According to today’s monthly Cattle on Feed report, USDA estimates that all cattle and calves on feed were 11.6 million head on Oct. 1, 2024, slightly below year-ago levels. Placements of cattle on feed were 2.16 million head, 2% below October 2023. Marketings of fed cattle were 1.7 million head, 2% above last year.

The report indicates there are still plenty of fed cattle for packers to choose from, which typically leads to lower cash prices. However, if the pattern of smaller placements compared to marketings continues, this should result in fewer cattle on feed. Strong production estimates agree with this scenario. Weather has the potential to play a major role in placements of cattle on feed over the next six months (more on this later).

Production

According to USDA’s October Livestock Slaughter report, September beef production was 2.2 billion pounds, up 3% from last year. The production estimates came from 2.57 million head of cattle, down about 1% from a year ago. The average live weight was record high at 1,406 pounds, 44 pounds higher than September 2023.

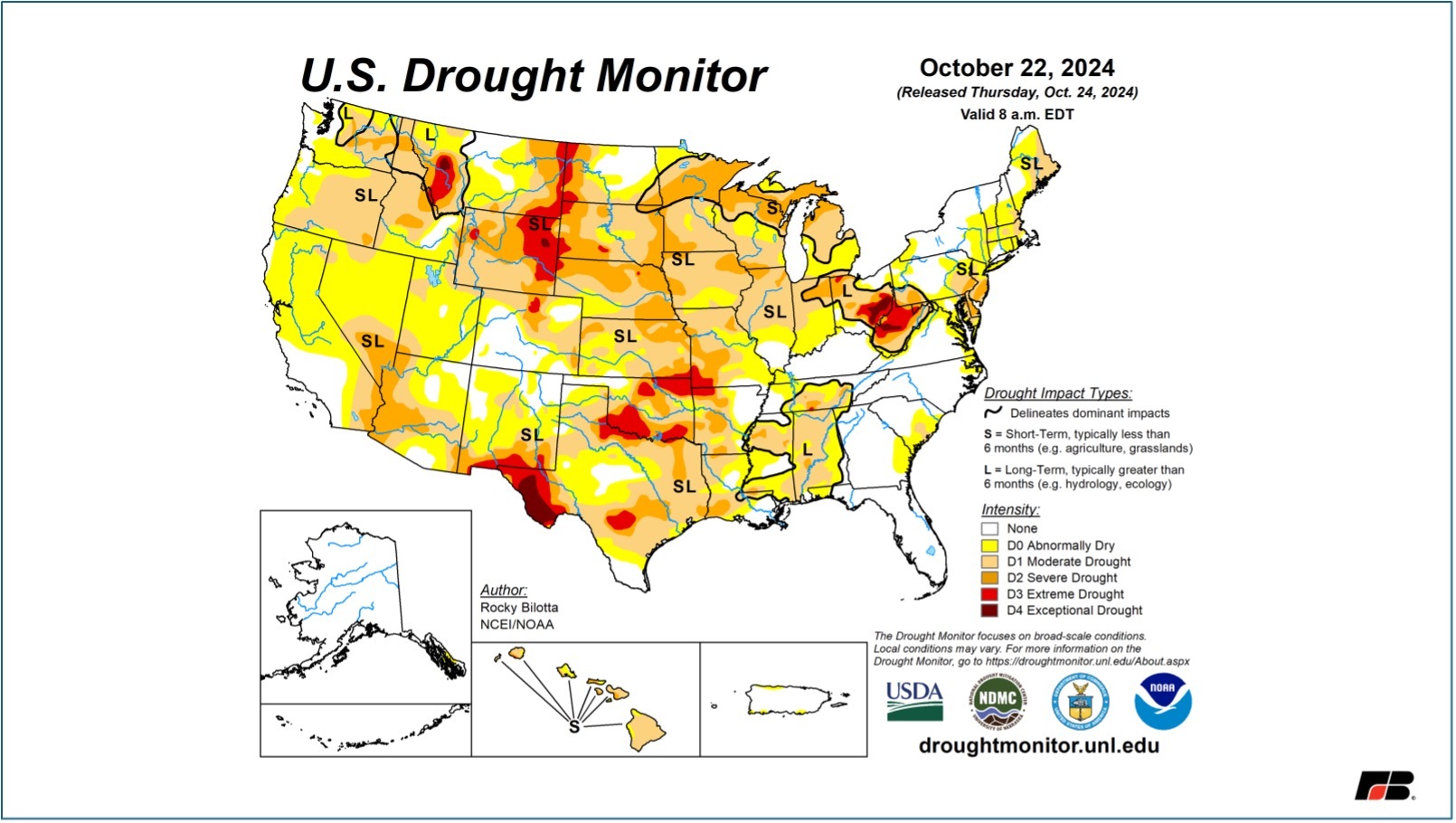

Heifers and cows made up about 47.8% of September slaughter volume, down from 51% in September 2023. This significant difference may be an indicator that some female retention is occurring. However, the U.S. Drought Monitorhas recently indicated emerging dryer conditions. The National Oceanic and Atmospheric Administration indicates there is a 60% chance of a La Niña developing and bringing dryer conditions to key cattle-producing regions of the country, likely elevating female cattle slaughter, resulting in continued cattle inventory contraction in 2025.

Conclusions

This week’s USDA reports indicate a strong number of cattle on feed. Plenty of cattle available for bidding means packers have to compete less to maintain profits. This can sometimes lead to lower cash prices. Beef production estimates align with slightly increased marketings of fed cattle and should keep beef moving from packers into the retail market. This is good news for consumers experiencing higher beef prices at the grocery store.

Without the July cattle inventory, it’s impossible to know what the spring calf crop looks like. Most analysts suspect the new calf crop is smaller than last year’s crop of 24.7 million head. However, the recent lower percentage of female slaughter could be an indicator that some female retention occurred in 2024. If this happened, the calf crop may come closer to even with last year’s estimates. Even so, it will be a year before female calves from this generation are ready to expand the cattle inventory with a calf of their own. And if emerging drought conditions continue, it is likely that placements of cattle on feed will rise further, reducing the overall cattle inventory.

Top Issues

VIEW ALL