Cattle on Feed Falling in Hypercycle

Bernt Nelson

Economist

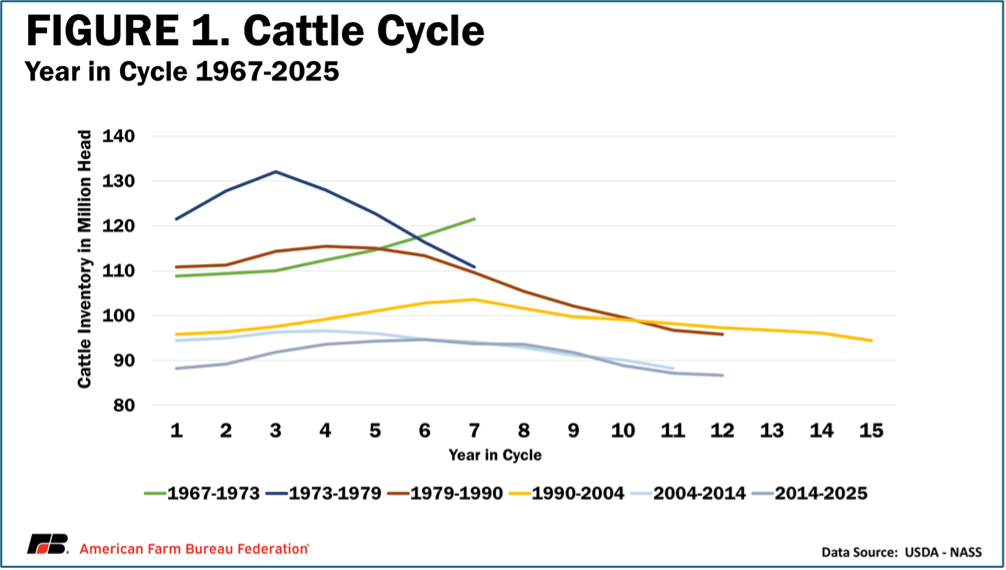

The cattle market moves in cycles, usually lasting nine to 10 years. The current cycle is already in its 12th year, including its seventh year of contraction, the longest since the 1990-2004 cycle. The current feedback loop of high prices and the sale of beef cows for slaughter instead of breeding is creating an unprecedented updraft, leading to record prices and leaving it anyone’s guess when the cycle might return to Earth.

Cattle on Feed

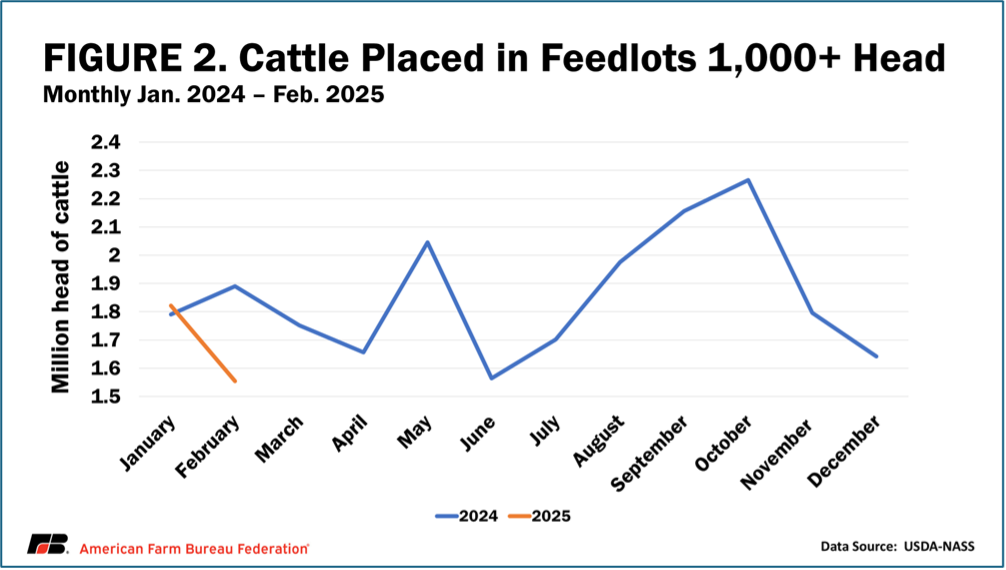

USDA estimated cattle and calves on feed on March 1 at 11.56 million head, down 2% from last year and slightly below average analyst expectations. (The monthly Cattle on Feed report measures cattle on feed in U.S. feedlots with capacity of 1,000 or more head as of the first of the month.)

This was a very bullish report. Placements of cattle into feedlots in February were 1.55 million head, 18% below the same time in 2024 and the lowest number for any month since June 2016. This drop was anticipated after months of elevated placements through 2024. Cattle available to be placed on feed have begun drying up and feedlot inventories have declined since the start of the year. This will lead to fewer fed cattle being available for beef production during the summer months when beef demand is typically the highest (Figure 2). This sharp decline could be the first sign of herd rebuilding and an indication that the current cattle cycle is coming to an end. However, this is not your typical cattle cycle.

Beyond the Average Cattle Cycle – A Hypercycle

The cattle cycle is the expansion and contraction of the cattle inventory as a response to farmers’ and ranchers’ perceived profitability of the beef cattle industry. Most cycles last about 10 years, but this is not your typical cattle cycle. The industry is now in its 12th year of the current cycle, and the seventh year of its contraction phase.

Multiple years of drought and deteriorating pasture conditions combined with high feed prices and inflation-driven supply costs are the major factors that drove farmers to sell their cattle, dropping the cattle inventory to a 73- year-low in 2024that continued through 2025. Now, drought is creeping into the picture again with some form of drought occurring in states where about 60% of the country’s cattle are raised.

Interest rates remain elevated, and inflation-driven supply costs have come down only slightly. Higher cattle prices are good for sellers but are less desirable for newcomers or the mid-career rancher looking to expand. According to USDA’s 2022 Census of Agriculture, the average farmer’s age has increased from 57.5 years old in 2017 to 58.1 years old in 2022. Now imagine a rancher near 60 years old with a cattle herd and good prices. The prospect of selling while prices are good is enticing compared to the alternative of taking on debt at high interest rates to maintain infrastructure or purchase expensive cattle with uncertain market conditions ahead.

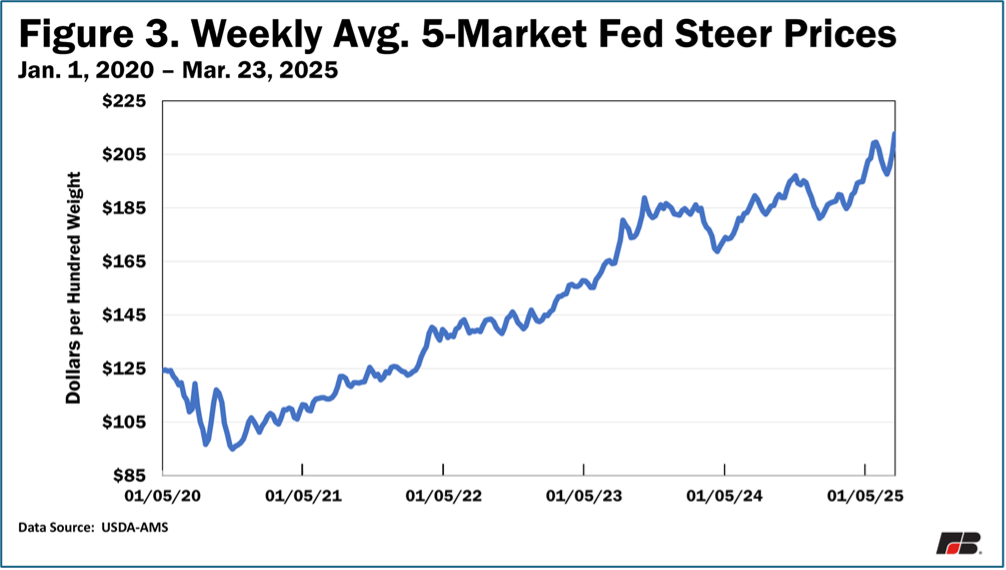

Going a little deeper, fed steer prices, along with prices for calves and feeder cattle, have been rising since 2020 and brought some much-needed profitability to struggling ranchers (Figure 3). USDA’s Cold Storage report estimates the quantity of meat and other products in U.S. warehouse freezers. According to the report released on March 25, beef in cold storage was down 6% from last month and 2% from last year. This slight decline in cold storage is evidence of continued strong demand. It also may indicate some buying to get ahead of any future export demand changes from tariffs. The packers that process beef are seeing this higher demand and sticky high prices for beef and are offering higher prices to the feedlots, who offer higher prices to ranchers for their cattle and calves.

In a normal cattle cycle, ranchers would see the best prices of their life and expand. However, today’s ranchers know these prices can’t be trusted to stick around, so they are sending some of their cows to market because they are worth more now than the calves they would produce will be worth in 18-24 months. Most ranchers won’t sell their entire herd, but they may sell enough to continue the tight supply and keep prices elevated. This could continue the feedback loop and sustain the contraction phase of this “hypercycle.”

Looking Ahead – Cattle Markets

Futures markets for both feeder cattle (700-900lbs) and live cattle (market ready) responded by dropping through Wednesday (March 26) afternoon, despite a strong opening on Monday (March 24). Futures markets are responding to economic anxiety, a softening stock market and the potential impact of tariffs. A weakening economy could mean weakening demand for beef. Tariffs, especially on our biggest trade partners, would further weaken export demand in the months ahead, if they triggered retaliation against our beef.

The cash market, on the other hand, remained very strong with the 5-area average price for live delivered steers at a record-high last week of $213.23/cwt. The choice beef cutout value rose $10.86 in just two days to $337.86/cwt on March 26. This was a massive move in price and is the highest cutout value since record prices were set in June 2023. These higher beef prices will be a test of demand, but they could also be a result of the strong consumer sentiment to get ahead of the looming tariff deadline. If demand for beef remains strong at these price levels, prices for cattle and beef will likely remain elevated as we move closer to grilling season when demand for beef traditionally peaks for the year.

Futures markets are indicating that cattle are worth more now than they will be later in the year. If trade isn’t disrupted, and domestic demand remains strong in grilling season, further contraction and elevated prices may continue. This trend would extend the contraction of the cattle inventory and keep this “hypercycle” alive.