Grills are Heating up Nationwide, and so is Demand for Beef

Bernt Nelson

Economist

Memorial Day is first and foremost a time for Americans to honor military personnel who died serving their country. It’s also the unofficial kick-off to summer – and grilling season, stimulating demand for all types of animal proteins, including beef.

Though the July Cattle Inventory has been discontinued by USDA’s National Agricultural Statistics Service, we can use other reports to piece together the cattle and beef market outlook. This Market Intel covers three beef reports to tell the story of where markets and grocery store prices are headed as we kick off grilling season.

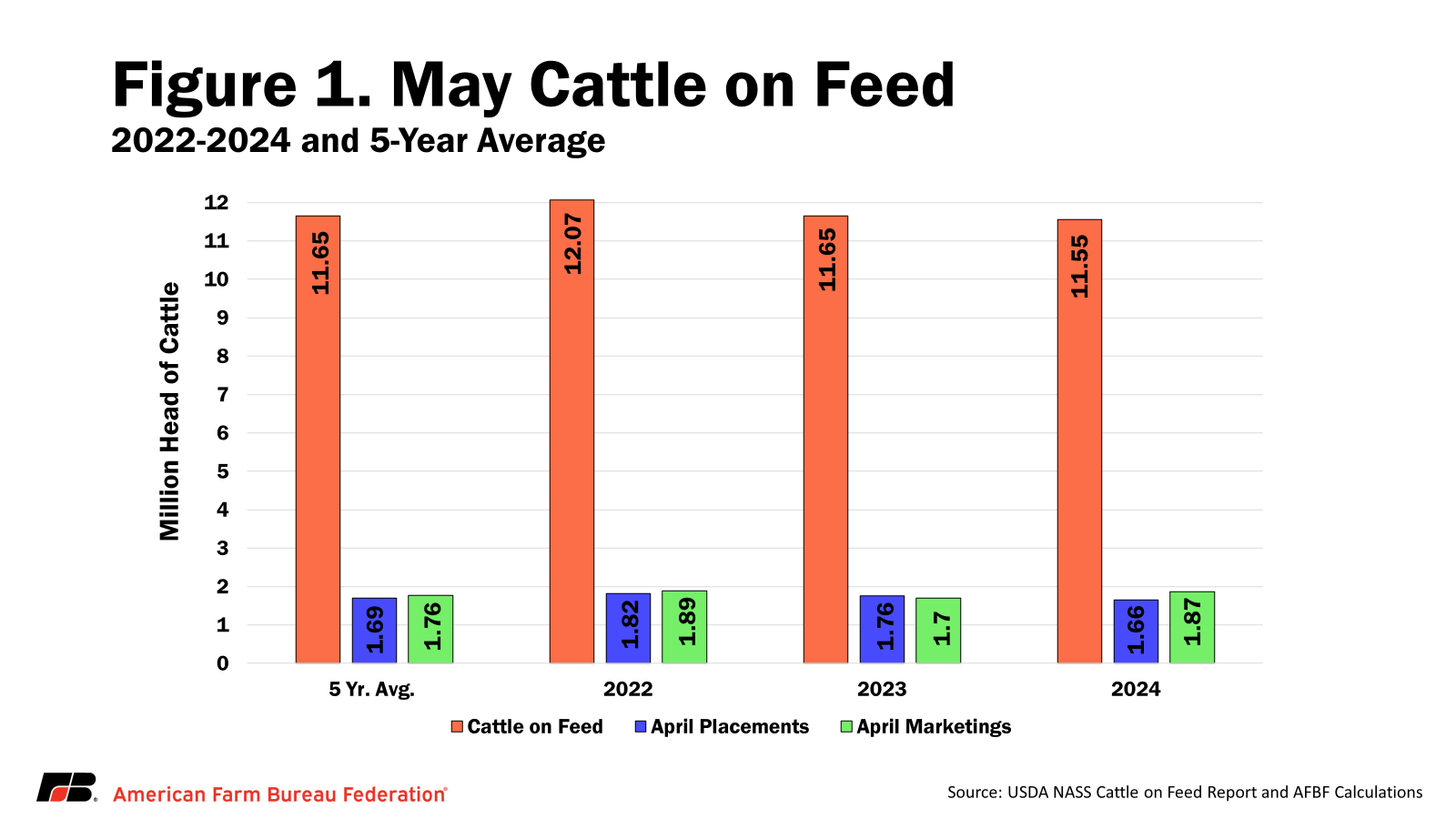

Cattle on Feed

USDA’s monthly Cattle On Feed report, published on May 24, estimates that there were 11.6 million head of cattle on feed on May 1, up 1% from May 2023. Cattle placed on feed in April were estimated to be 1.66 million, down 6% from April 2023. Cattle marketed in April totaled 1.87 million head, up 172,000 head or 10% from 2023. Cattle on feed for 120-plus days was 4.72 million, down 4.5% from last month, but up about 5.5% from this time last year. This still leaves higher numbers of fed cattle available in the short run and should help keep beef prices from skyrocketing through the summer.

Substantial improvements in drought conditions over the last year, especially in parts of the country with high concentrations of cattle, could result in more cattle being retained for breeding purposes rather than being placed on feed. If this happens, placements could fall through the remainder of 2024 as cattle feeders continue to add weight to what they already have in feedlots rather than adding more cattle.

Regardless of the reason for fewer cattle on feed, the result is the same: fewer cattle available for beef production in the long run.

Livestock Slaughter

NASS’ monthly Livestock Slaughter report, released on May 23, shows April 2024 beef production was 2.3 billion pounds, up 234 million pounds, or 11%, from April 2023. Average live weight was 1,395 pounds, up 41 pounds from April 2023. This is just 6 pounds less than the record average live weight of 1,401 pounds set in December 2023. Cattle prices are up from last year, increasing the cost for packers to buy market-ready cattle. Increasing production during a time of high retail prices helps packers make up for paying more for cattle.

Cold Storage

Also released on May 24 was USDA’s monthly Cold Storage Report, a helpful tool in gauging the amount of nearly 150 different items kept in cold storage, including beef. USDA estimates beef in cold storage on April 30 was 413.95 pounds, down 1% from last month and down about 16.7 million pounds, or 5%, from last year. All red meat in freezers totaled 955.9 million pounds, which is about 9% below year-ago levels. Increased production addressed earlier in this article has helped keep beef in cold storage from dropping more rapidly. There have been some record prices set for beef products early in 2024, but increased production has kept most national average retail prices from hitting record levels so far this year.

Prices and Demand

USDA’s May Livestock, Dairy, and Poultry Outlook provides additional data useful in analyzing beef supply and demand. This report forecasts 2024 U.S. per capita disappearance of beef will be 58.3 pounds per person, an increase of 0.2 pounds from 2023. However, USDA is projecting this metric will fall by 5%, to 55.6 pounds per capita in 2025. Much of this decrease is due to expected consumer fatigue from inflation and expected record beef prices in late 2024 and 2025.

Summary and Conclusions

While there is no substitute for the data provided in NASS’ July Cattle Inventory survey report, especially for projecting the next 12 months of supply, other USDA reports can be used to ascertain the overall direction of the market as we head into the summer grilling season and the peak beef demand that comes with it.

The May Cattle on Feed report estimated lower placements of cattle on feed – normal for this time of the year – and higher marketings. In addition, much-needed moisture is helping improve pasture conditions across the country, giving farmers a reason to retain heifers for breeding purposes. While this would be the first step to expanding the U.S. beef herd again, a smaller 2024 calf crop projected by USDA means the first opportunity for expansion of the cattle inventory will not occur until 2025. Domestic demand for beef is still strong but tight supplies will continue to drive up grocery store prices through 2025, which will drive down consumer demand for beef, according to USDA forecasts.

Farm Bureau July 4th Cookout Survey

The results of the American Farm Bureau Federation’s Fourth of July cookout cost survey, which will be released on June 26, will provide a grassroots snapshot of the cost of beef and other traditional Fourth of July favorites.