Prospective Plantings Report Shows Big Shift to Corn

Betty Resnick

Economist

Despite the immense uncertainty in agriculture due to the escalating trade war, farmers do not have the luxury of delaying planting decisions – or planting itself. Now that spring has arrived, they will soon head to the fields to put this year’s crop in the ground.

The 2025 Prospective Plantings report surveyed nearly 74,000 farmers between February 27 and March 18 on what they intend to plant this year. As expected, due to market conditions and a large dip in acreage last year, farmers are intending to plant significantly more corn, moving away from cotton, wheat and soybeans.

Corn. Corn. Corn.

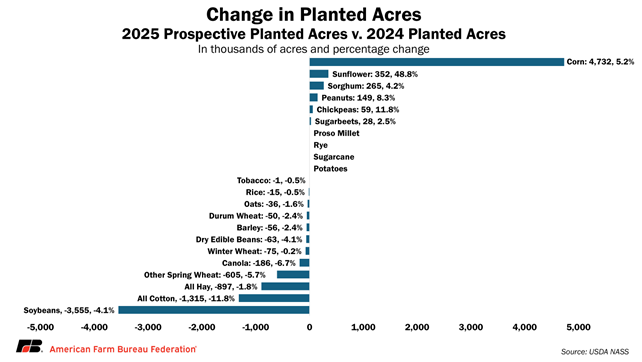

The main take away from the Prospective Plantings report is that we’re planting corn – a lot of it. Farmers intend to plant 95.3 million acres of corn in 2025, a 5.2% increase of 4.7 million acres compared to corn planted last year. This figure came in above most, but not all, trade estimates and 1.3 million acres above USDA’s projection at February’s Agriculture Outlook Forum. If realized, planted corn acres would be the third highest since 1944 and the highest since 2013.

Corn is taking acres from many crops, with the largest swings in total acres away from cotton and soybeans. If realized, at 30.8%, corn would be at its highest-ever percentage of principal planted crops since at least 1993, when the total principal crops planted metric was first available from USDA’s National Agricultural Statistics Service.

Swings in Planted Acreage

On an acreage basis, soybeans (4.7 million acres) and cotton (1.3 million acres) had the largest acre declines from 2024 planted acres. On a percentage basis, cotton is projected to have the biggest decrease at -11.8% to only 9.9 million acres, the lowest planted acres in over a decade. Cotton has been facing very poor profitability for several years now and is among the crops with the highest percentage of production exported, making it very vulnerable to retaliatory tariffs. All forms of wheat also have projected decreases in acres including other spring wheat (-5.7%, -605,000 acres), durum (-2.4%, -50,000 acres), and winter wheat (-0.2%, -75,000 acres).

Besides corn, sunflowers have the largest projected increase in acres, recovering to 1.1 million acres with an additional 351,700 acres (48.8%) compared to last year, when sunflower production was historically low. In addition to corn at 5.2%, peanuts (8.3%, 149,000 acres) and chickpeas (11.8%, 59,000 acres) have the next largest increases in intended acreage.

Total Principal Crops Planted Acres

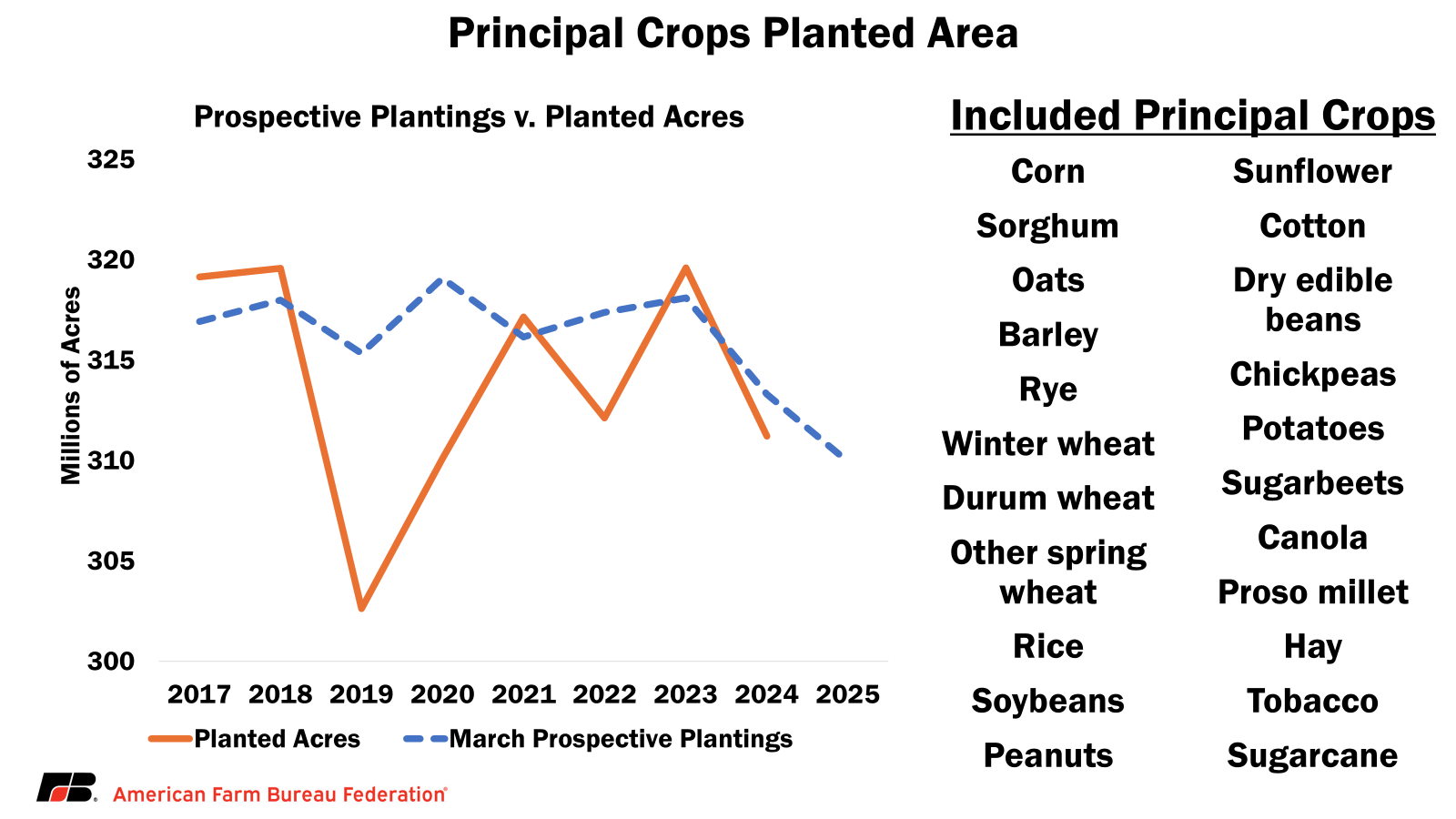

USDA’s definition of principal crops includes 22 crops ranging from corn to potatoes to proso millet. In 2025, USDA is again projecting a drop in intended planted acres for total principal crops, falling to 309.9 million acres, down 1.3 million acres (-0.4%) from 2024’s final planted acres. It is also the smallest March intended planted acres for principal crops since the metric was introduced in 2017, and the first time that we have seen back-to-back years of reductions in March intended planted acres – with a decline of nearly 10 million (-3%) from the acres planted in 2023.

As we look into the third year of potentially negative crop returns for several crops, is it possible that farmers are starting to reduce acres due to economic conditions? Are they shifting toward unaccounted for crops? Are they putting the land into conservation programs? Is it land now being used for non-farming purposes, like residential or solar development? I raised some of the same questions last year from the prospective planting report, but they are potentially even more relevant today.

Quick Note on Grain Stocks

Also published was one of our four Quarterly Grain Stock reports. Unsurprisingly, the report confirmed that corn stocks are down slightly (-2.4%) from this time last year, soybeans are slightly up (3.5%) and wheat is up significantly at 13.6%.

Takeaways

The March 31 NASS reports, including Quarterly Grain Stocks, Rice Stocks and the Prospective Plantingreports, brought no surprises. As expected, corn acres are up due to the relative strength of corn compared to other commodity prices. As we continue in a period of increased uncertainty for farmers due to potential policy changes in trade and biofuels, the table is set as we move into planting season.

Also, as a reminder to farmers, the ARC/PLC deadline for 2025 is April 15. If you have not yet made your way to the Farm Service Agency office to confirm your decisions for 2025, it would also be a good time to apply for the Emergency Commodity Assistance Program, which has an application open through August 15.