Ukraine, Russia, Volatile Ag Markets

Veronica Nigh

Senior Economist

Though a distant second for now to the humanitarian crisis brought on by the Russian invasion of Ukraine, the market volatility occurring along with it has many worried about how rising commodity prices will affect those outside of the region.

As is well known, Ukraine is a powerhouse producer and exporter of some key agricultural products. The country is a market mover in the crops and countries in which it trades, so disruptions in the Ukrainian market are having ripple effects across the world. The growing global concern is that the prolonged absence of Ukrainian products on the global market will lead to additional suffering in the form of food price crises in countries not directly involved in the conflict. We dig in here.

Ukrainian Agriculture

Ukraine is a significant producer and exporter of agricultural products. In 2021, Ukraine exported more than $27 billion in agricultural products to the world. Ukraine’s top export markets were the 27 nations that now comprise the European Union (EU-27) at $7.6 billion, China at $4.2 billion, India at $2 billion, Egypt at $1.5 billion and Turkey also at $1.5 billion. These top five markets accounted for more than 60% of Ukraine’s agricultural exports. Ukraine has six primary products with over a billion dollars in export sales: corn ($5.8 billion), sunflower seed ($5.7 billion), wheat ($5.1 billion), rapeseed ($1.7 billion), barley ($1.3 billion) and sunflower meal ($1.2 billion). Combined these top six products accounted for more than 77% of Ukraine’s agricultural exports.

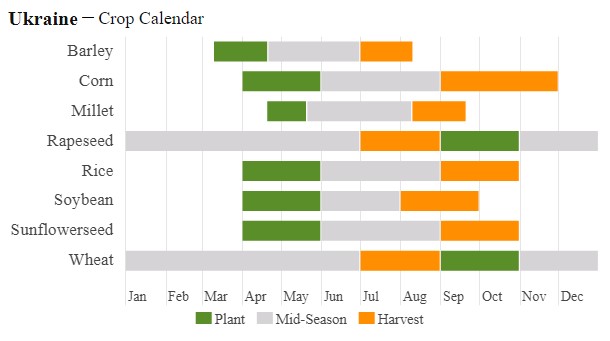

As the assault on Ukraine stretches on, the impacts to Ukraine’s ability to produce the volume of tradeable commodities the global market has grown to depend on will become more significant. A substantial part of Ukraine’s most productive agricultural land is in its eastern regions, exactly those parts most vulnerable to Russian attacks. The climate and soils of Ukraine have been likened to that of Kansas, Minnesota and North Dakota. And as with farmers in those states, farmers in Ukraine plant most crops in April and May, except wheat and rapeseed, which were planted in September and October and are now in the growth phase.

Not only will an ongoing war likely lead to fewer planted acres, but it is also likely to change the mix of crops that will be planted and harvested. With a heightened focus on feeding the Ukrainian people, it is likely that farmers will be encouraged to plant and harvest crop cereals intended for local consumption, rather than corn, sunflower seed and rapeseed for export. As reported by Reuters, Denys Marchuk, deputy head of the Ukrainian Agrarian Council, told local television, "The emphasis will be on spring crops that will be harvested in the summer, because we do not know what the situation will be (going forward). For the full nutrition of its population and the armed forces, more emphasis will be placed on buckwheat, peas, those types of crops that will make it possible to harvest so that Ukraine is fully provided with food."

In the case of crops yet to be planted, as well as the wheat and rapeseed crops already in the ground, farmers will be challenged to find fuel for their machinery and fertilizer for their fields, which will likely reduce the total harvest on planted acres. It cannot be underscored enough that Ukrainians are under mortal threat; the situation goes well beyond disruptions to business as usual for Ukraine’s farmers. Predicting what and how much will be planted by farmers living in daily fear for their lives feels insensitive, but a deeper understanding of Ukraine’s top export crops can help explain the extreme market volatility of the last several weeks and potential risks to the larger world.

Corn

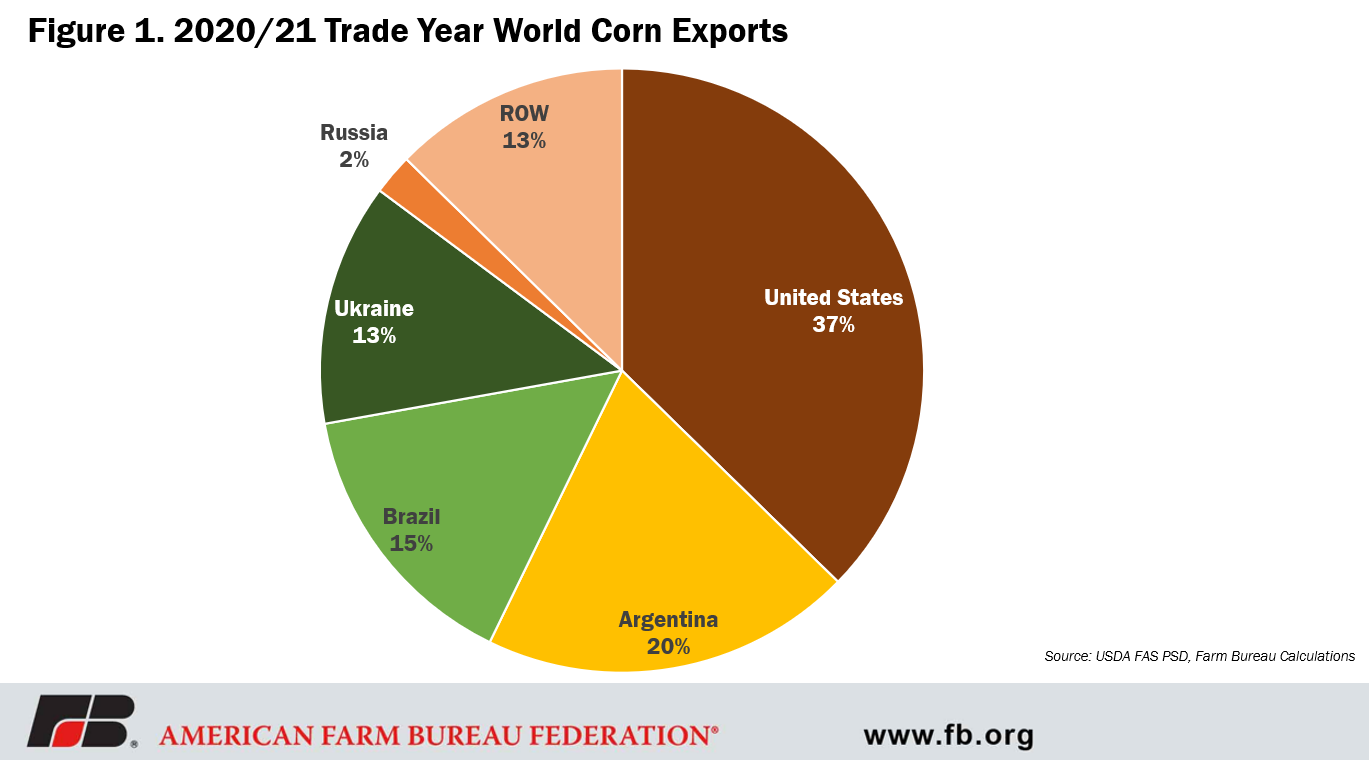

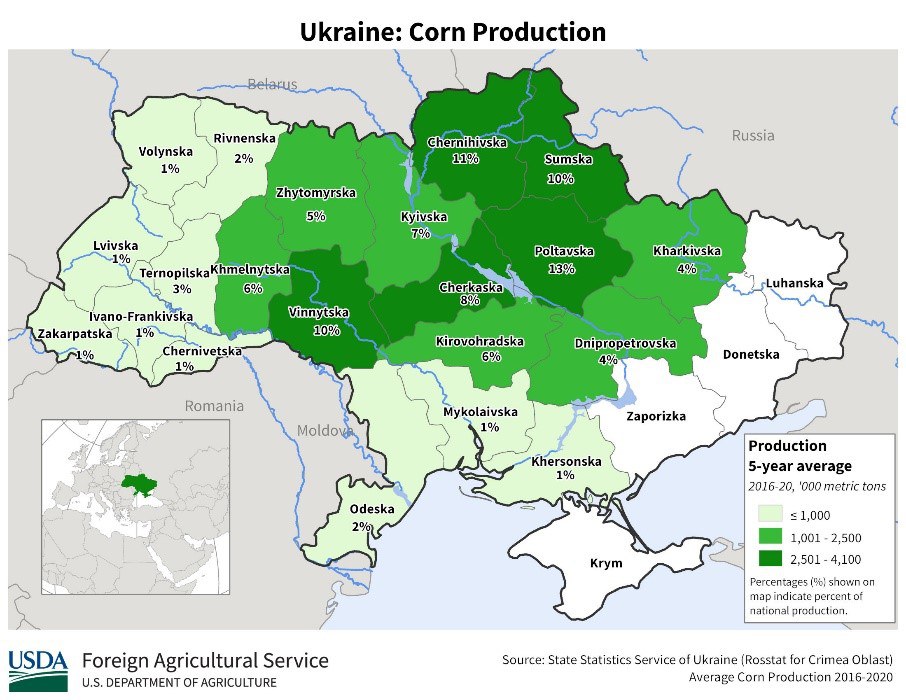

Ukraine is the world’s seventh-largest producer and fourth-largest exporter of corn, responsible for 13% of global exports in the 2020/21 growing year. The crop is predominantly grown in the northern half of the country, with a concentration in the northeast, (including Chernihivska, Sumska and Poltavska, visible on the map below) where approximately 35% of the country’s corn is grown.

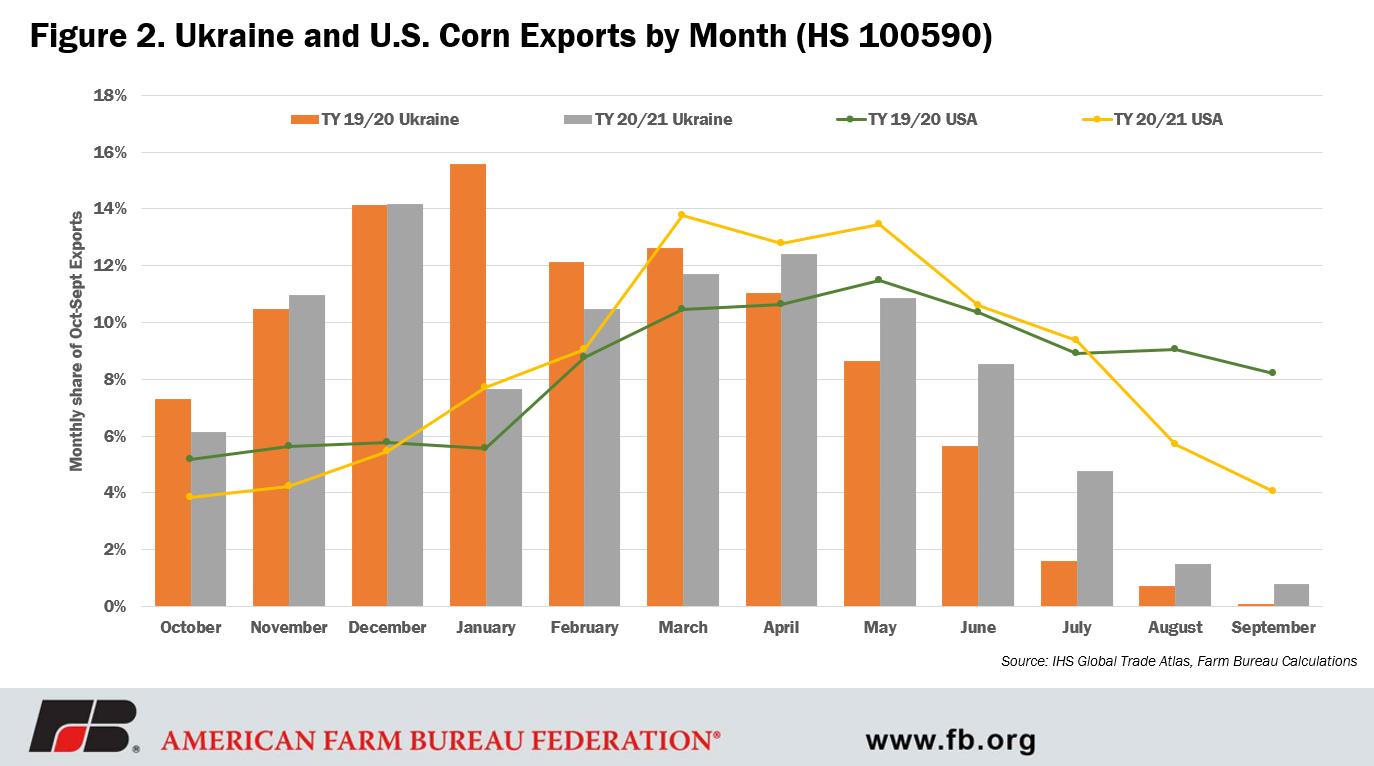

Ukraine exported more than $5.8 billion in corn to the world in 2021. China ($1.9 billion) and the EU-27 ($1.8 billion) were the top two destinations for Ukrainian corn, accounting for more than 60% of corn exports. Ukrainian corn growers are trade dependent; over the 17/18 – 20/21 trade years an incredible 80% of Ukraine’s corn production was exported. Despite similar growing seasons, Ukrainian corn is exported primarily between November and May, while U.S. corn exports are strongest between March and June. For the global market that means that relatively large stocks of trade year 21/22 Ukrainian corn remain stuck in-country after the closure of Ukraine’s Black Sea ports. The March WASDE estimated Ukraine corn exports at 27.5 million metric tons. According to S&P Global Ukraine had exported 18.98 million mt as of February 23. This means that there are over 8.5 million mt still remaining to meet the USDA's export estimate for this marketing year. There has been discussion of utilizing Ukraine’s state-run rail system to move the 8.5 million metric tons of Ukrainian corn to borders with Romania, Hungary, Slovakia and Poland, from where the grain can be delivered to ports and logistics hubs of European countries.

The Chinese and European markets are as reliant on Ukrainian corn imports as Ukrainian corn farmers are on those export markets. In 2019, the EU-27 imported $4.6 billion in corn from the world, 63% of which was sourced from Ukraine. Brazil was a distant second, supplying 20% of the EU’s corn market. In 2021, China imported nearly $8 billion in corn from the world. The U.S. was China’s largest supplier in 2021 with 70% of the market, but Ukraine was still a significant supplier. China imported 29% of its corn crop from Ukraine in 2021, valued at more than $2.4 billion. In recent years, Ukraine commanded a larger share of China’s corn imports. Over the 2016-2019 period, Ukraine’s market share averaged 77%.

Wheat

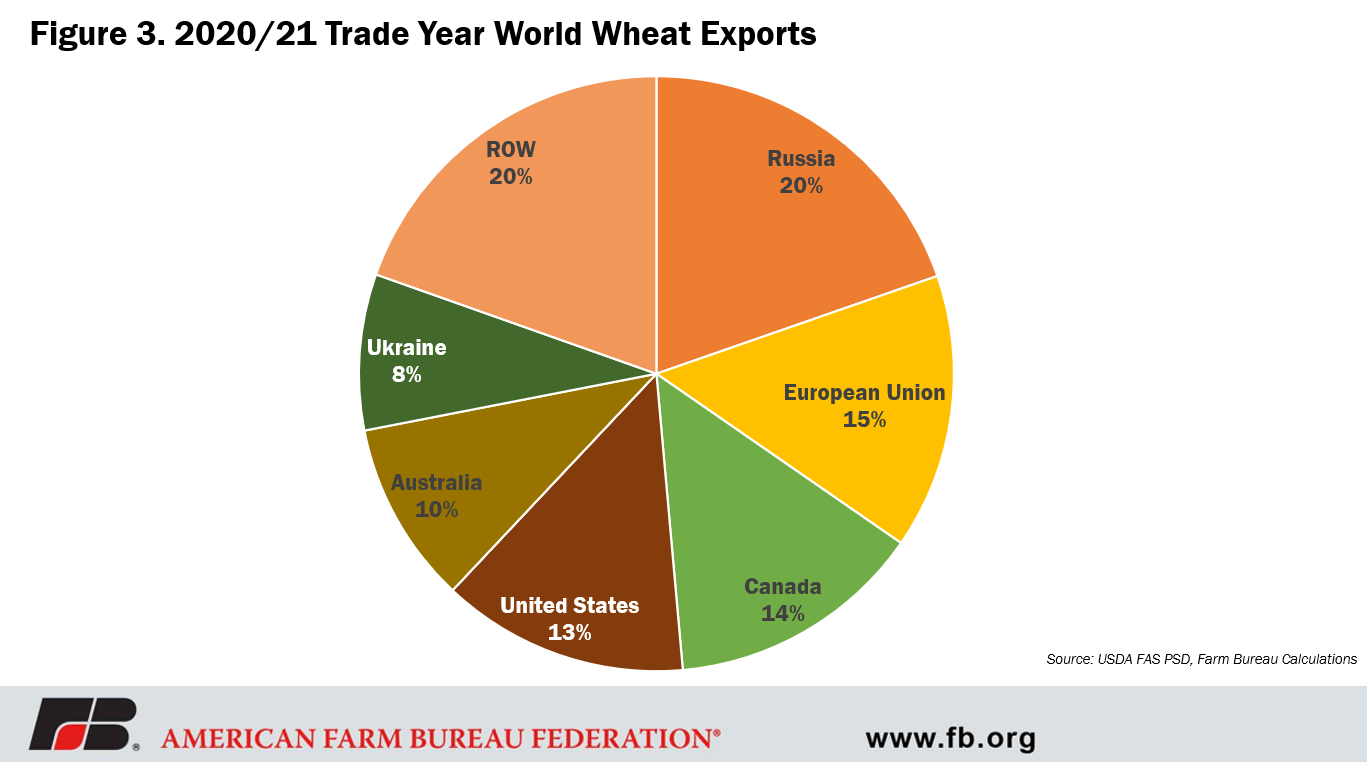

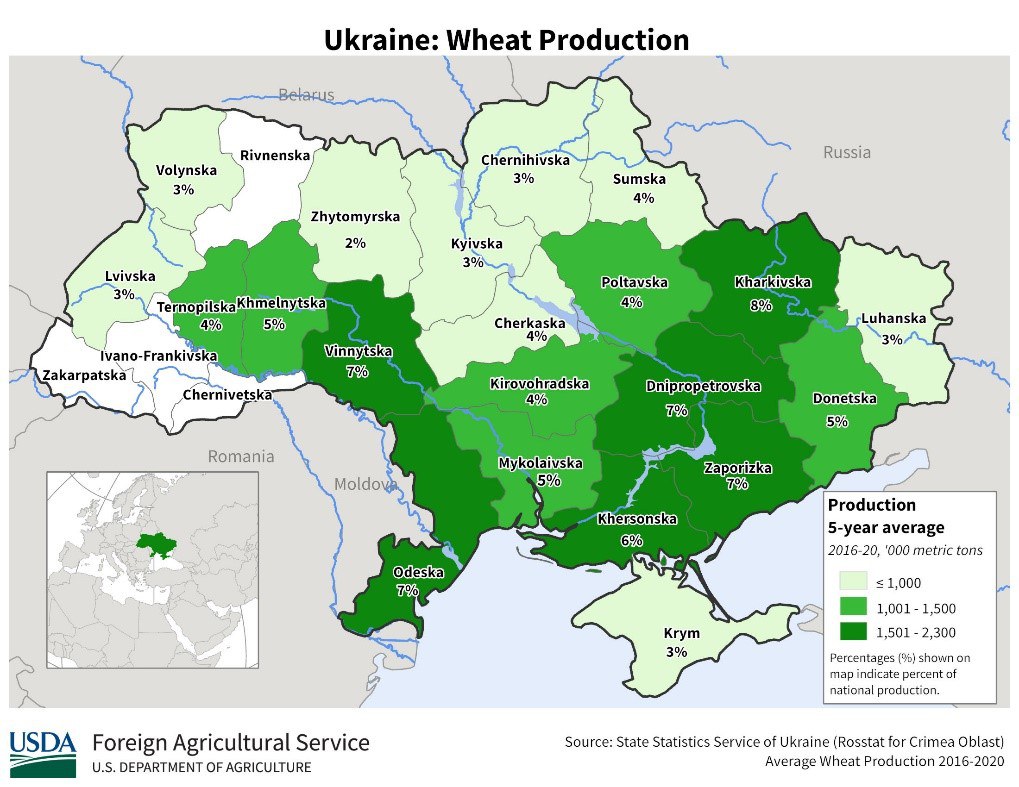

Ukraine is the world’s eighth-largest producer and sixth-largest exporter of wheat, responsible for 8.5% of global exports in the 2020/21 trade year. The crop is predominantly grown in the southern/southeastern portions of the country. Ukraine’s wheat growing season is like the winter wheat growing season in the United States, with planting occurring in September and October, growth throughout the winter and spring and harvest occurring in July and August.

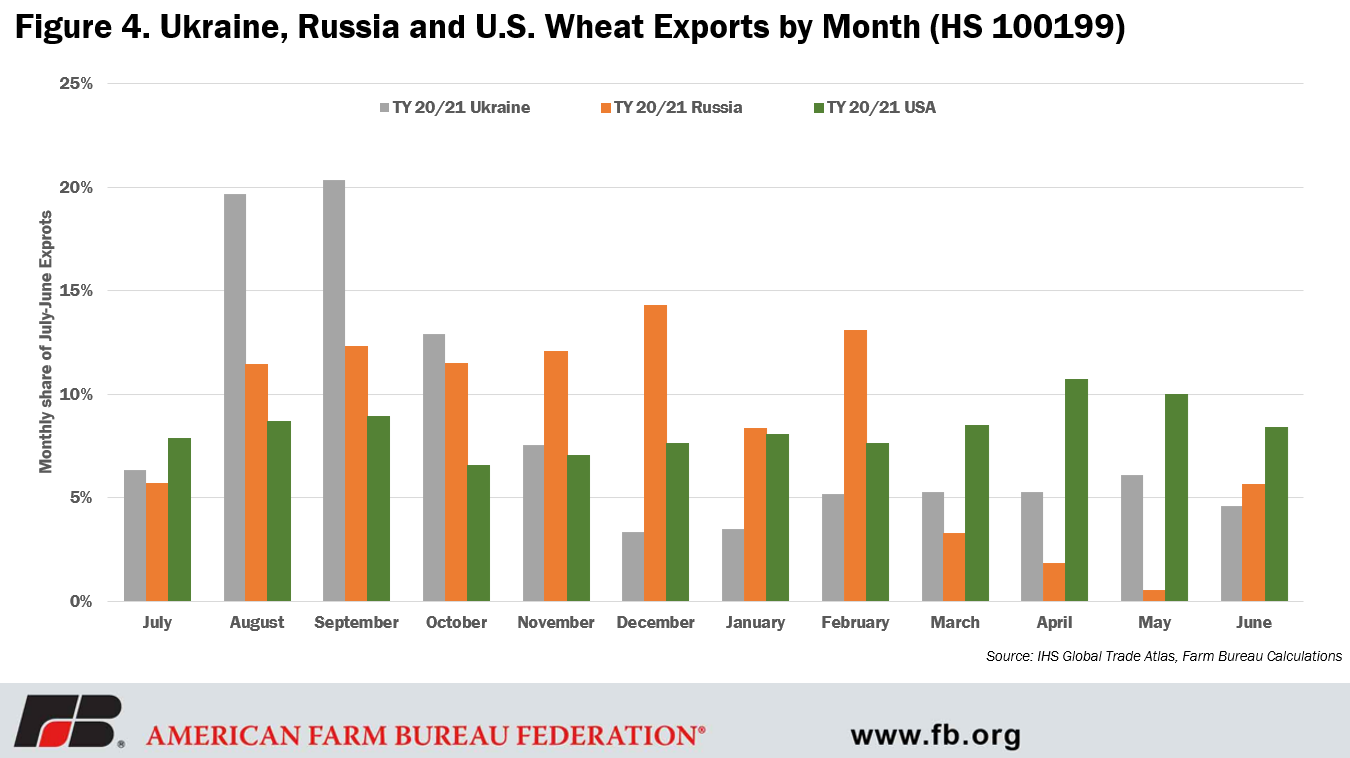

Ukraine exported nearly $5.1 billion in wheat to the world in 2021. Top destinations for Ukrainian wheat are completely different than that top destinations for Ukrainian corn. In 2021, the top destinations were Egypt ($858 million), Indonesia ($727 million), Turkey ($445 million), Pakistan ($353 million) and Morocco ($232 million). These top five markets accounted for nearly 50% of Ukraine’s wheat exports. Unlike the U.S. wheat export campaign, which is steady throughout the year, Ukrainian wheat is primarily exported between August and November.

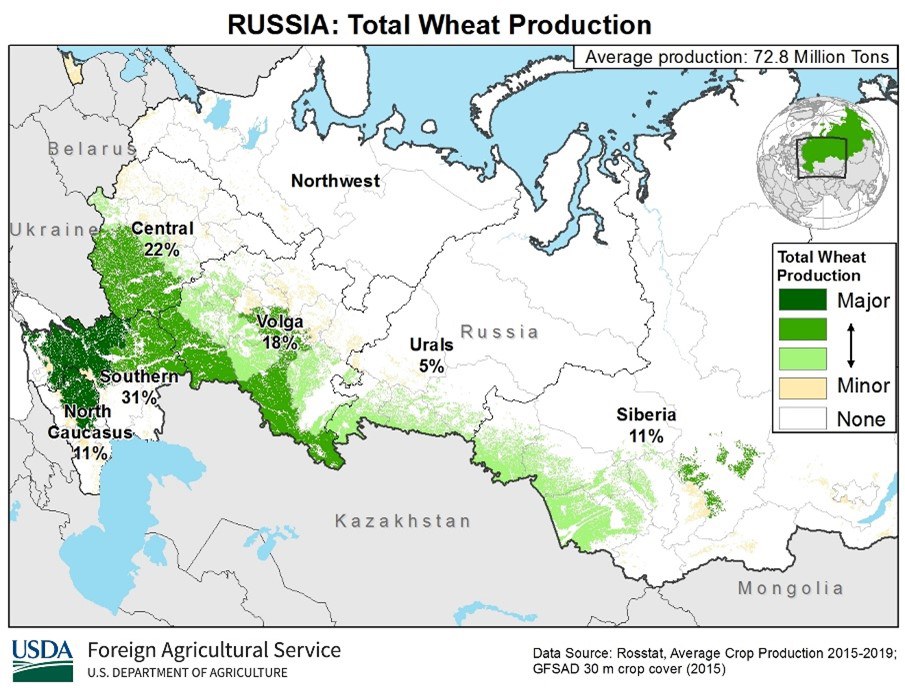

In addition to the significant production and exports of wheat in Ukraine, Russia is an even larger supplier. In the 2020/21 trade year, 20% of the world’s wheat exports came from Russia. Together, these two countries accounted for nearly 30% of the globe’s wheat exports. Russia’s export campaign is more like Ukraine, beginning in August, but stretching longer, into February. This means that both Ukraine and Russia have completed the bulk of their trade year 2021/22 wheat exports.

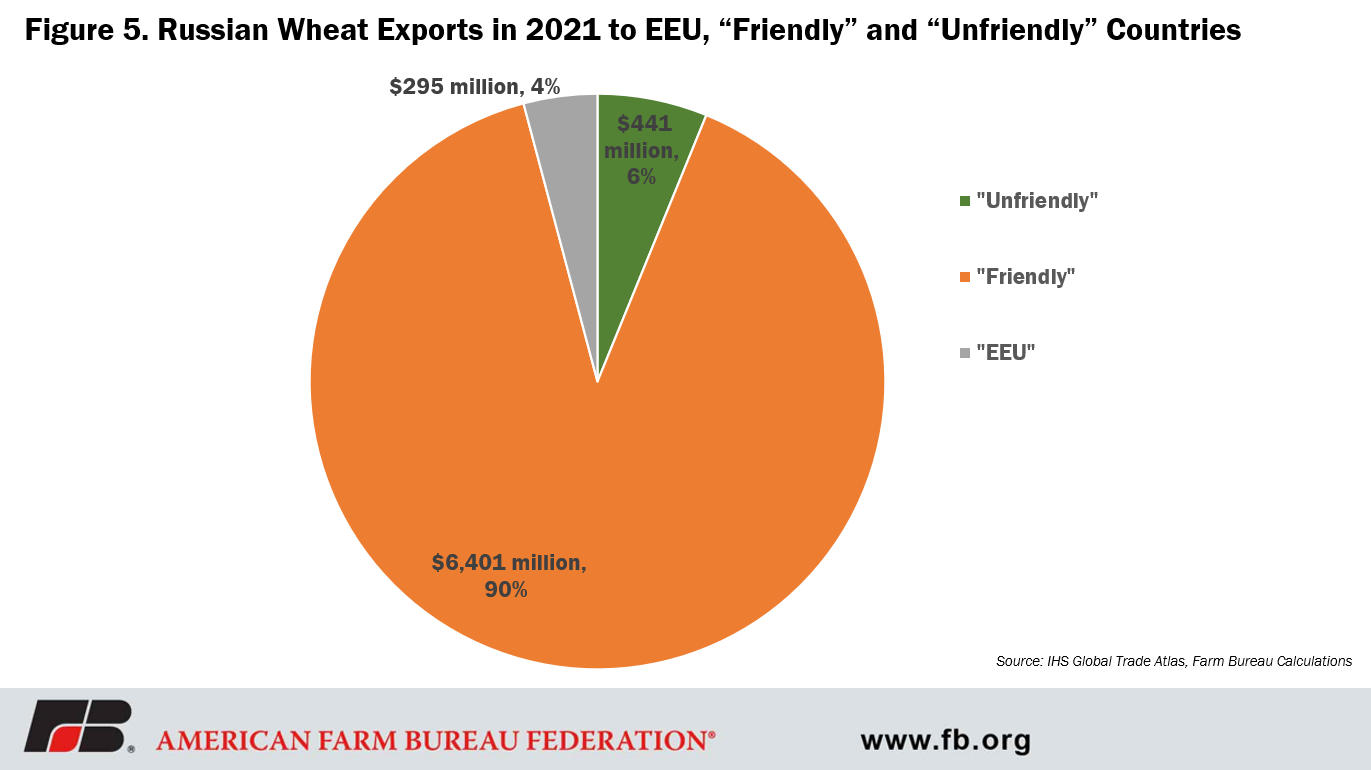

In response to Russia’s invasion of Ukraine, several Western countries have introduced a series of measures to try to hobble the Russian economy. Many Western governments, including the United States, have imposed strict sanctions on Russian banks, elites and exports, and major international companies have suspended their Russian operations. In retaliation, on March 10, Russia announced a ban on exports of telecom, medical, auto, agricultural, electrical and tech equipment, as well as some forestry products, to about 48 countries that have "committed unfriendly actions" against Russia, including the U.S. and the EU, until the end of 2022. Russia exported more than $7.1 billion in wheat to the world in 2021. While the export ban may be significant for some products, like fertilizer, which will be discussed below, only 6.2% of Russia’s 2021 wheat exports were to countries “guilty” of committing “unfriendly actions.” However, a few days later, on March 14, Russia announced a temporary ban on the export of wheat, rye, barley and corn to Eurasian Economic Union nations, which include Armenia, Belarus, Kazakhstan, and Kyrgyzstan, ex-Soviet countries. This temporary ban is significant because these four countries are all ex-Soviet countries, but only 4.1% of Russia’s 2021 wheat exports were to the EEU. So, while Russia represents a significant portion of global wheat exports, the threat of Russian wheat export disruptions will be the result of lower production from diverted resources and/or physical damage due to military movement through the primary growing region, which borders Ukraine, not the export ban as it is currently defined.

Vegetable Oils

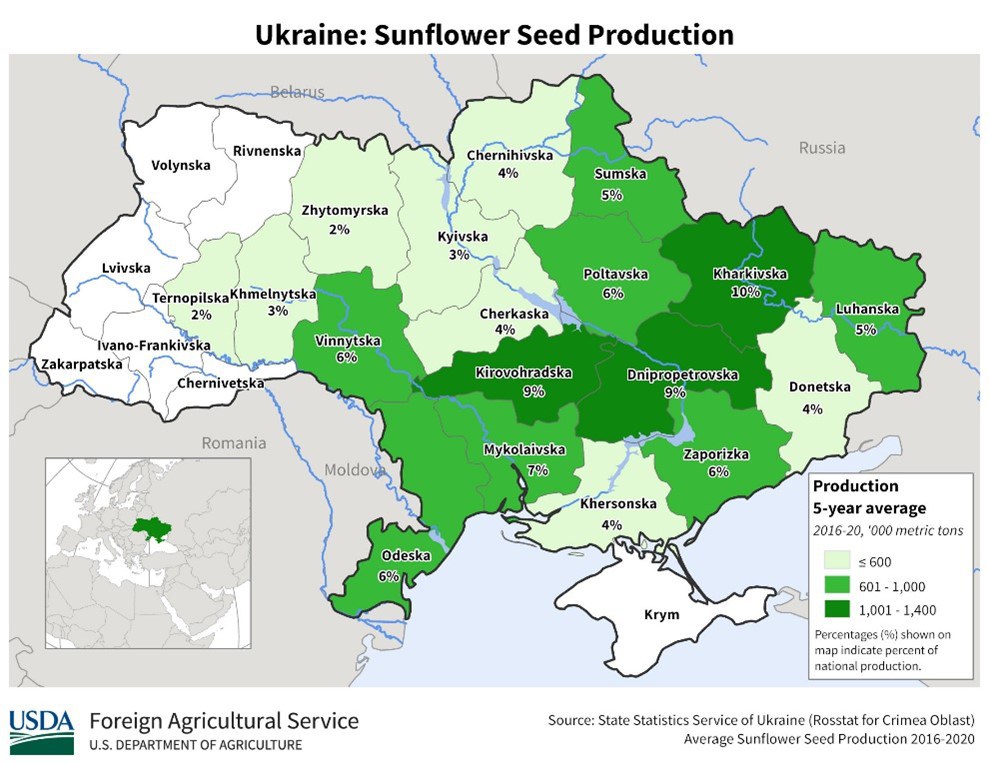

Ukraine is the world’s largest producer and exporter of sunflower seed and its products, responsible for 47% of global exports in the 2020/21 trade year. The crop is predominantly grown in the eastern half of the country. Ukraine’s sunflower crop is planted in April and May with a September and October harvest.

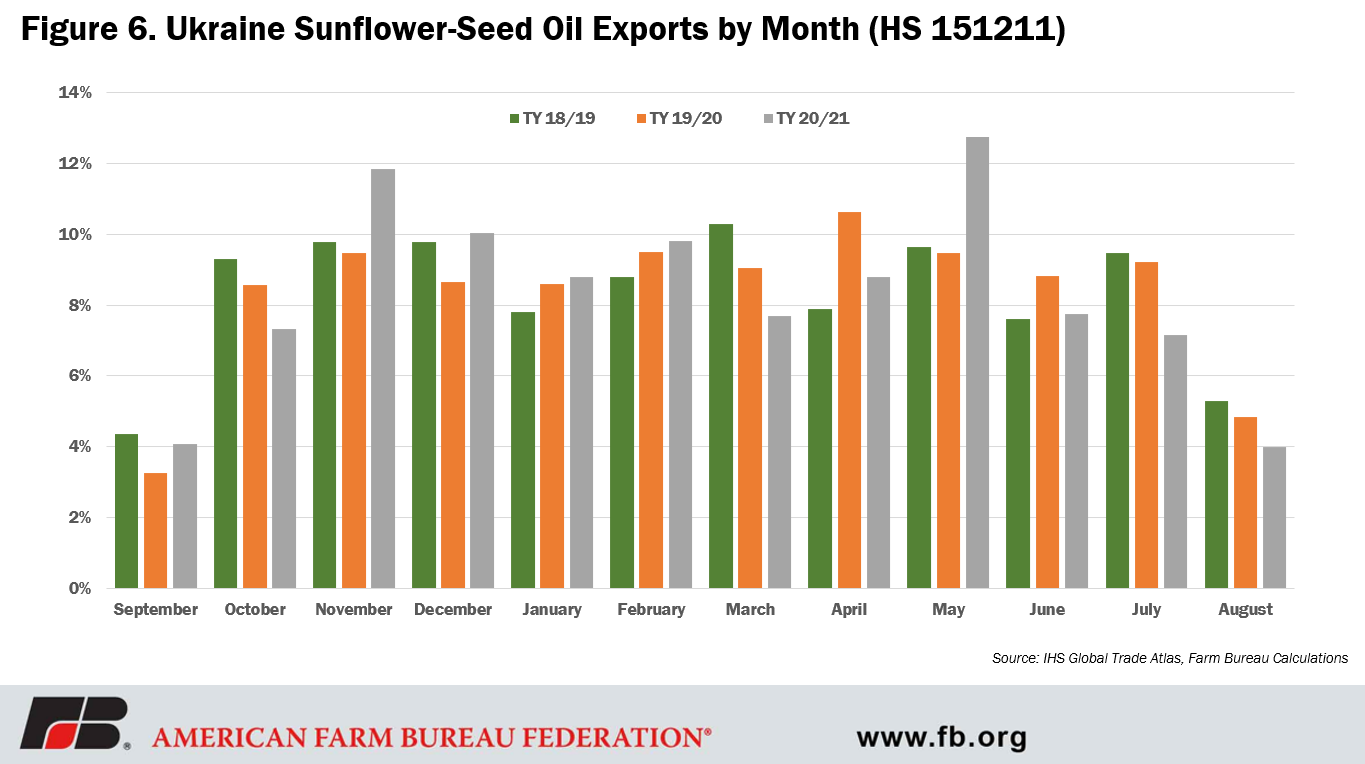

Ukraine exported nearly $5.7 billion in sunflower oil to the world in 2021. Top destinations for Ukrainian sunflower seed oil were India ($1.9 billion), EU-27 ($1.7 billion), China ($872 million) and Iraq ($313 million). These top four markets accounted for more than 85% of Ukraine’s sunflower seed oil exports. The export campaign for sunflower seed oil is steady throughout the year except for August and September. Like corn, this means that a lot of exportable sunflower seed oil remains in Ukraine. This product will hang over the market in the coming months, with sunflower seed oil prices likely varying considerably on rumors of movement and quality of exportable Ukrainian supplies. Reduced global sunflower seed oil trade will continue to exert upward pressure on substitute vegetable oils, like soybean oil.

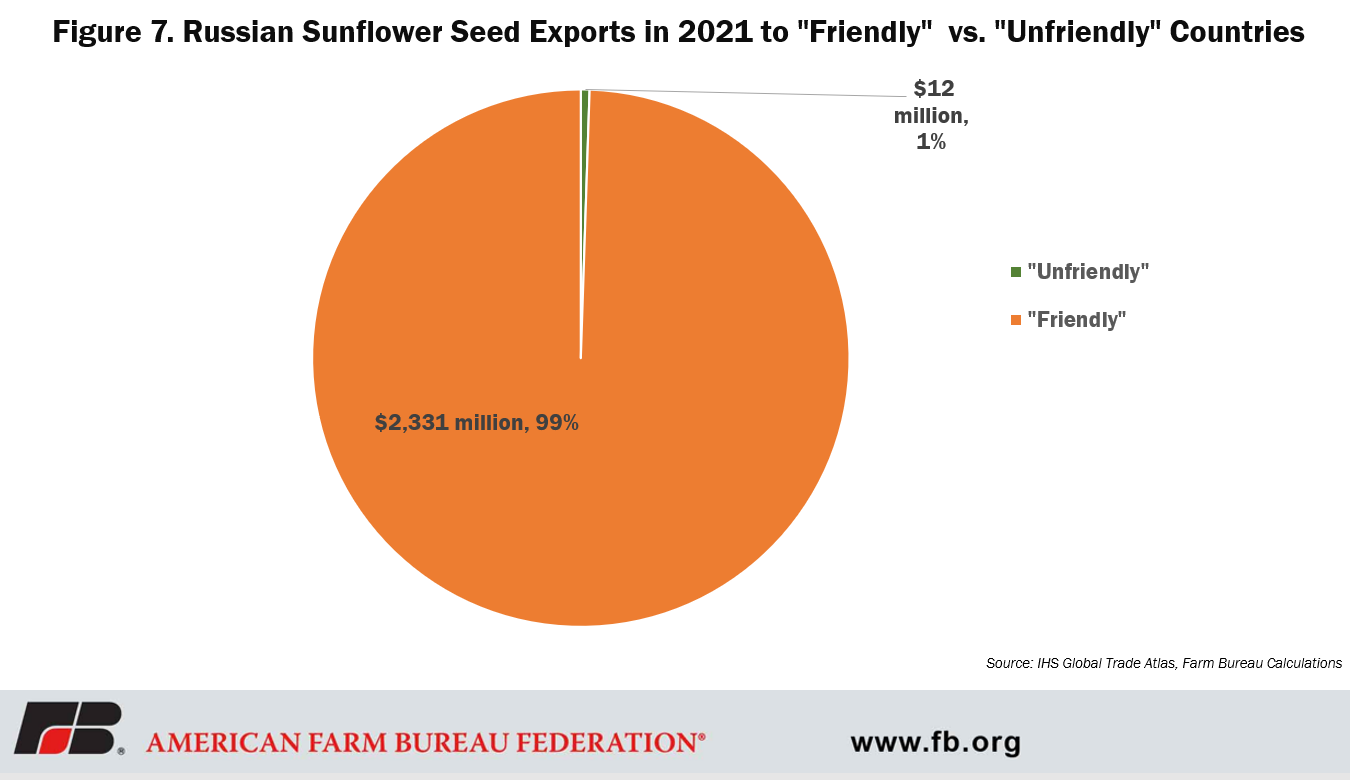

In addition to the significant production and exports of sunflower seed oil in Ukraine, Russia is also a significant supplier. In the 2020/21 trade year, 29% of the world’s sunflower seed oil exports came from Russia. Together these two countries accounted for over three-quarters of the globe’s sunflower seed oil exports. Like wheat, Russia’s exports of sunflower seed oil are predominantly to countries that will not be impacted by Russia’s export ban. Only $12.2 million, merely 0.5%, of Russia’s $2.4 billion in sunflower seed oil exports in 2021 were to countries “guilty” of committing “unfriendly actions.” Again, while Russia represents a significant portion of global sunflower seed oil exports, the threat of export disruptions from Russia will be the result of lower production from diverted resources and/or physical damage due to military movement through the primary growing region, which borders Ukraine, not the export ban as it is currently defined.

Fertilizer

The availability and price of fertilizer has been a top concern of farmers around the world for months. Russia’s invasion of Ukraine has only complicated already challenging global fertilizer markets. Western sanctions and Russia’s retaliatory export ban have taken Russia, a significant producer and exporter of fertilizer, out of many countries’ markets. Russia is a major global player in all three nutrients that compose fertilizer: nitrogen, phosphate and potassium. Russia is the world’s largest nitrogen exporter, supplying 16.5% of global nitrogen exports in 2018, the most recent year for which data is available. Russia is the world’s third-largest phosphate exporter with a 12.7% share of global phosphate exports in 2018. Russia is the world’s third-largest potassium exporter as well, supplying 16.5% of global potassium exports in 2018. Unlike the situation described above with respect to wheat and sunflower seed oil, Russia is a significant source of fertilizer imports for many of the countries on the “unfriendly” list. Fertilizer is a highly traded, global commodity. Forty-four percent of all fertilizer materials are exported. The division of the world’s fertilizer importers, which are basically all counties that grow anything, into two groups – those that are “friendly” and those that are “unfriendly” - will make accessing fertilizer more expensive and more difficult.

Energy

The large influence Russia has on energy markets is well known. Russia is the world's third-largest oil producer, the second-largest crude oil exporter and the largest exporter of oil. Russia is the second-largest natural gas producer, after the U.S., the second-largest exporter of natural gas in gaseous state and the fifth-largest exporter of liquified natural gas in 2019. Energy is big business to Russia. According to an article from The Associated Press, before the invasion, Russian oil and gas made up more than a third of government revenues.

To date, Russia’s list of banned exports does not include energy products, but that does not mean Russia’s energy exports have continued on unaffected. Because of Russia’s invasion of Ukraine, many Western countries (some of those “unfriendly actors” Russia is upset about) have sanctioned Russia’s largest banks, its central bank and finance ministry, and moved to block certain financial institutions from the SWIFT messaging system for international payments, which has made Russia’s trade of energy more difficult and expensive. Last week, the U.S. announced a ban on Russian energy. Though Russia only made up about 3% of U.S. oil imports last year and the U.S. does not import Russian natural gas, the move was seen as an act necessary to isolate Russia economically. Allies in Europe have announced plans to become less dependent on Russian energy, though that transition will take time. Europe is not a significant producer of energy and depends heavily on imports. Russia supplies 40% of Europe’s gas and 25% of its oil.

Russia will play a lot of games in the energy markets in the coming weeks and months. Expect an extended period of disruption. And because natural gas accounts for 70-90% of the cost of nitrogen fertilizer, that market will continue to trade in turbulent waters for some time to come as well.

Infrastructure

Beyond the markets discussed above, a critical piece of the Ukraine puzzle will be the level of damage that its infrastructure sustains during the Russian invasion. Once the fighting has concluded, in what condition will they find their roads, bridges, rail lines and ports? Significant damage to any segment of infrastructure will make moving people and products more time consuming and more expensive.

Global Food Prices – Where it All Comes Together

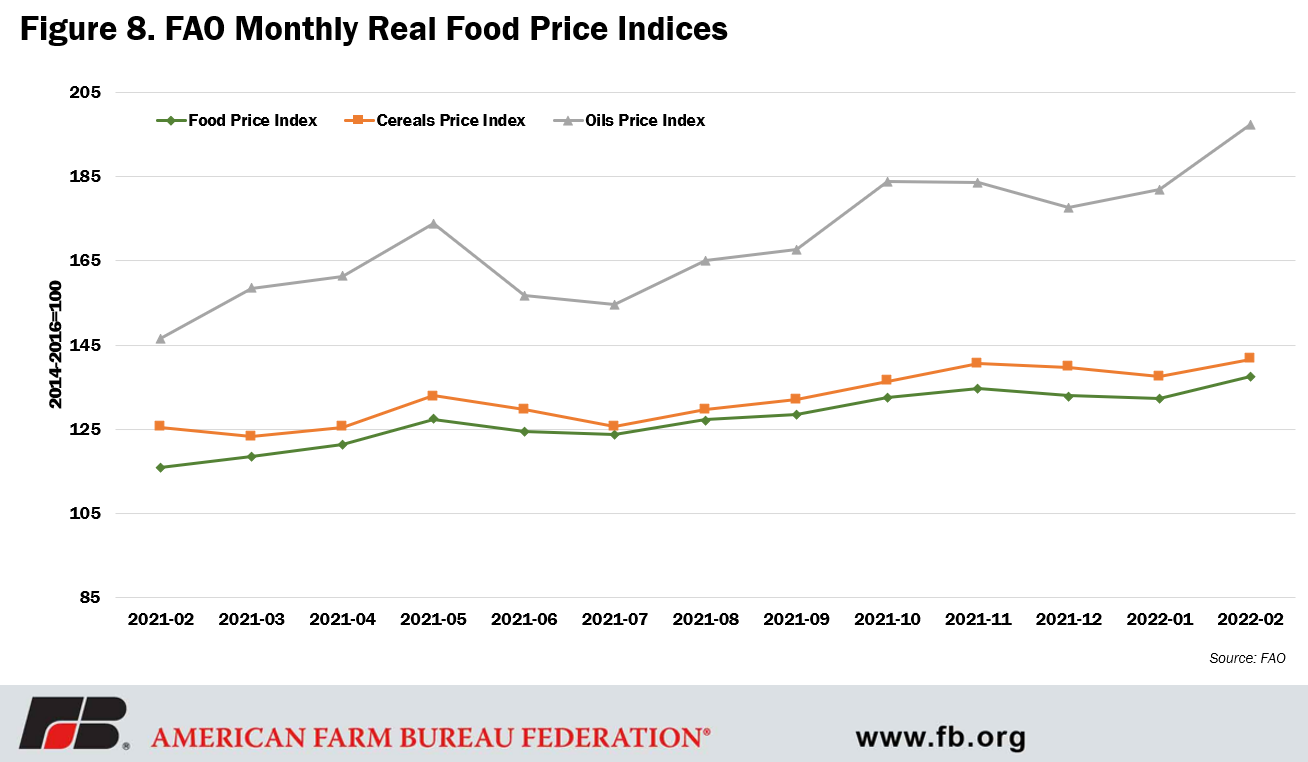

The world has been justifiably focused on the plight of Ukraine’s citizens, but as Russia’s assault wears on, there has been a growing concern about the impact on people beyond Ukraine’s border because of increased global food prices influenced by reduced global supplies of wheat, corn and sunflower seed oil. The Food Price Index (FFPI) from the United Nations’ Food and Agriculture Organization is a measure of the monthly change in international prices of a basket of food commodities. The FFPI measures price changes for five commodity groups relative to 2014-2016. Those five commodity group price indices are then weighted by the average export shares of each of the groups to give an overall change in the overall market basket. The FFPI is released each month, allowing policymakers a real-time barometer of the global marketplace.

The FFPI adjusted for inflation averaged 137.6 points in February 2022, up 5.2 points (3.9%) from January and as much as 21.6 points (18.7%) above February 2021. According to the FAO, this represents an all-time high. The FAO Cereal Price Index adjusted for inflation, which includes wheat, corn, sorghum, barley and rice, averaged 141.7 points in February, up 4.1 points (3%) from January and 16.2 points (12.9%) from February 2021. In February, prices of all major cereals increased from their respective values last month. In addition to corn and wheat discussed above, Ukraine is also a significant exporter of barley. The FAO Vegetable Oil Price Index adjusted for inflation, which includes palm, soybean and sunflower oil, averaged 197.3 points in February, up 15.4 points (8.5%) from January and 15.4 points (34.5%) from February 2021.

With the situation in Ukraine continuing to unfold, it is unlikely that the upward trajectory of food prices is over. And as prices rise, more and more people around the world will be challenged by food insecurity. Let us join in the chorus for peace in Ukraine.

What We're Saying

Trump Administration Pauses Reciprocal Tariffs for 90 Days

Apr 10, 2025

READ MORE ![]()

U.S. Imposes Reciprocal Tariffs on Trading Partners

Apr 3, 2025

READ MORE ![]()

Retaliatory Tariffs Placed on Agricultural Goods

Mar 18, 2025

READ MORE ![]()

Tariffs on Mexican, Canadian Goods Put into Effect

Mar 4, 2025

READ MORE ![]()