Understanding the New Tariffs

TOPICS

tariffs

Betty Resnick

Economist

Trade has become a hot topic this year, with a lot of uncertainty. Trade policy decisions being made in Washington will impact farmers and ranchers in the countryside. This Market Intel report is part of a series exploring different topics related to agricultural trade, including the potential impacts of trade policy changes: Agricultural Exports 101 and Tallying Up the Latest Retaliatory Tariffs.

President Trump’s sweeping new tariffs, introduced on April 2, will alter the American economy. Following an announcement speech, Trump signed two executive orders, one implementing “reciprocal” tariffs and another removing tariff exemptions from relatively low-value shipments from China (the “de minimis” exemption). This Market Intel will detail what we know to date about the new tariffs.

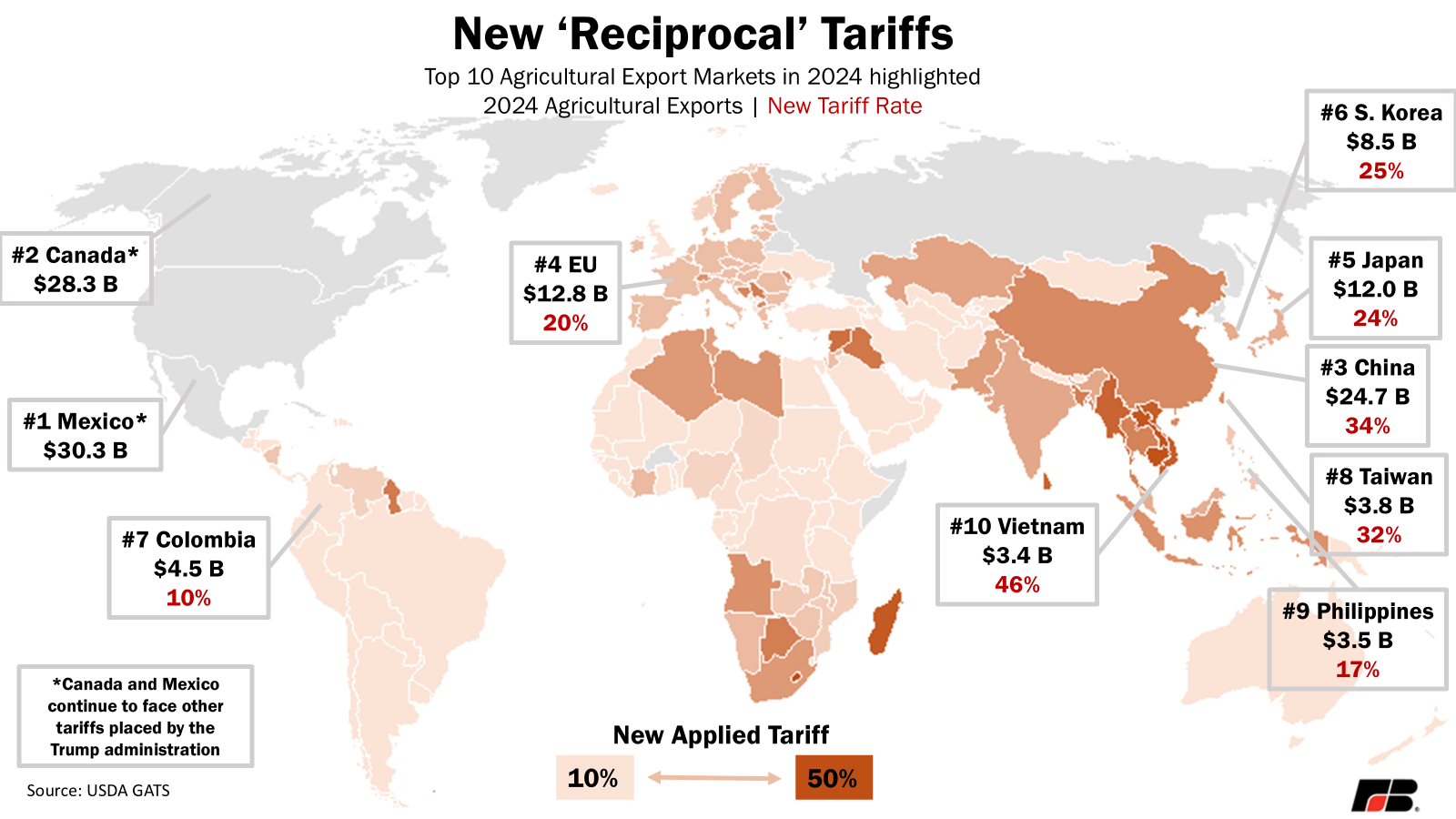

What are the Tariffs?

Starting on April 5, a 10% baseline tariff will be applied to nearly all products from all countries, with a few notable exceptions explained later. The executive order’s Annex I lists 57 countries (83 when accounting for all European Union member states) that will face higher tariffs of up to 50%, which go into effect on April 9. The new tariffs will stack on previous product-specific tariff rates. As a reminder, a tariff is a tax paid at the border by an importer seeking to bring products into the United States from a foreign country.

According to the Office of the United States Trade Representative. the new tariffs were calculated by taking the value of the trade balance in goods divided by the value of U.S. imports of goods from the relevant country divided by two. The formula assumes that if two countries do not have a trade balance in goods (trade in services were not accounted for), there must inherently be tariffs, barriers or unfair trade practices causing the uneven trading relationship.

This formula penalizes a handful of very small countries. For example, the country with the highest tariff rate is Lesotho, a mountainous, landlocked nation slightly smaller than the state of Maryland and surrounded by South Africa. It has a population of only 2.3 million people and, in 2023, had a real GDP per capita of $2,600 (compared to $74,600 for the United States), ranking 202nd in per-capita GDP out of 222 countries according to the CIA Factbook. In 2024, Lesotho exported $237 million of products to the United States, of which 99% were clothing apparel and diamonds.

Notably, our new 34% tariff on China stacks on top of other tariffs we’ve already applied on Chinese products including 20% in response to their role in the production and distribution of fentanyl. Combined, Chinese products now face a 54% baseline tariff when imported into the United States.

Are any Countries Exempt from the New Tariffs?

Canada and Mexico are our top trading partners and the top two destinations for our agricultural products. For now, they are carved out from any new tariffs. Instead, the 25% tariff related to fentanyl/migration issues on non-U.S.-Mexico-Canada Agreement (USMCA)-compliant products remains in effect while USMCA-compliant products still enter tariff-free. The executive order does lay out that if the fentanyl/migration-related tariffs were to be repealed, they will be replaced by a 12% tariff on non-USMCA-compliant goods with energy/energy products, potash and eligible USMCA-compliant goods continuing to be duty-free. Previously announced tariffs, including 25% on all automobile, steel and aluminum imports, still apply to Canadian and Mexican imports with some questions lingering over implementation specifics.

Several countries left off the reciprocal tariff breakdown chart posted on X by the White House face other economic sanctions, including Russia, Belarus, North Korea and Cuba. Iran, which also faces steep economic sanctions, was on the list. Additionally, the White House did not clarify why Burkina Faso and Somalia were excluded.

Are there any Exemptions or Exceptions for Specific Products?

The exempted items in Annex II include, but are not limited to: copper, pharmaceuticals, semiconductors, lumber articles, certain critical minerals, energy/energy products, and products facing section 232 tariffs from the current administration (steel, aluminum, automobiles and any future section 232 investigations). While some of these industries were exempted due to their important roles in the economy (energy and critical minerals), others were excluded as they are a target for future restrictions (copper, lumber, pharmaceuticals and semiconductors).

For the agricultural industry, there are a few exemptions impacting inputs including veterinary vaccines (and all pharmaceuticals for humans too), several pesticide ingredients under HS 2399, fertilizers containing potash, peat, lubricating oils and greases, and other energy products.

Exemptions under “HS Chapter 31: Fertilizer" would have covered 44% ($3.8 billion) of all $8.7 billion in fertilizer imports in 2024. Exempted fertilizers include potash in many forms, including all potassic fertilizers under HS 3104 and several compound fertilizers containing potash under HS 3105, including “HS 3105.20 Fertilizers Containing Nitrogen, Phosphorus & Potassium” (i.e., NPK). All USMCA-compliant fertilizers from Mexico and Canada continue to enter duty-free.

Tariffs Hit Farmers’ and Ranchers’ Imports and Exports

Farmers and ranchers, like all Americans, will be paying more for many of the products they purchase, from seed for vegetable growers to tractors and other equipment made of steel. Some exemptions for products including potash and peat as mentioned above, which were hard fought for by agricultural organizations such as the American Farm Bureau Federation, are a testament to the effectiveness of farmers' and ranchers raising their collective voice. Analysis by the Tax Foundation reports the tariffs applied in 2025 will result in an average tax increase of more than $1,900 for every U.S. household annually, which, if correct, would be the largest tax hike in 43 years, if negotiations are not initiated and resolved quickly.

Retaliatory tariffs imposed by our trading partners make American products more expensive than products from countries not facing such tariffs, thereby lowering demand for the more than 20% of U.S. agricultural production that is exported. Before the tariff announcement on April 2, Canada and China already had retaliatory tariffs on $27 billion of U.S. agricultural exports. As of April 4, China, our third-largest agricultural export market, has already announced an additional 34% retaliatory tariff on all U.S. exports effective April 10. As new retaliatory tariffs stack on top of old ones, the total applied tariff for agricultural products in China will rise even higher. For example, the total retaliatory tariffs rise to 71.5% for soybeans, 74% for in-quota cotton and 99% for frozen swine offal. With the simultaneous increase of input prices and decrease in demand, farmers who are already in financial distress will further feel the squeeze.

Longer-term, farmers may also see demand reduction as our economy struggles to cope with these major changes. The volatility of the tariff policy decisions, with new tariffs frequently being announced, paused and placed will take a toll on the American agricultural industry, as on the rest of the economy. Farmers and ranchers suffer from instability, as their soundest business decisions can be turned upside down. If these tariffs lead rapidly to new agreements with new market access, they may help our farmers. In the meantime, without direct support from USDA or a farm bill with an updated safety net, farmers will almost certainly bear the brunt of these tariffs, as they always seem to do.